Diamond Backtesting

with

Walk Forward Manager

(BTWFMgr)

the

new cutting edge in Backtesting

sharp and clear like a diamond

by

Professional

Software Solutions

(Burkhard

Eichberger)

http://www.ProfSoftware.com/bt

Copyright ã

2004-2017 by Burkhard Eichberger. All rights reserved.

No part of this book may be reproduced in any form or by any electronic or

mechanical means including information storage and retrieval systems

without permission in writing from the author (pss@poboxm)

(BTWFMgr Version 3.X)

Table

of Contents

Fully automated advanced Walk

Forward Analysis (WFA)

Innovative Volatility Analysis

Advanced Strategy Input Parameter

Analysis

Position Profit/Loss Distribution

Analysis

Innovative Trading Strategy

Potential Analysis and Optimization

Identify the best Weekdays and

Entry Intraday times

Detect the Market Long/Short Bias

Detect the Strategy Trading

Frequency

Find the best exit logic - Position

Exit Manager (PEM):

Visual Multi Timeframe/Symbol

Analysis - Result Overview Module

Integrated In depth Performance

Analyzer (PerfAna)

Export Results to Microsoft Access

Database

Correlate Context Values with best

Potential

Automated modification of your

EasyLanguage Strategy Code

Equity/Walk Forward Mode

(nBTWFMgrExport=2)

Potential Mode (nBTWFMgrExport=1)

Data Collection turned off

(nBTWFMgrExport=0)

BTWFMgr Configuration and

Preferences

Step1 – Strategy Preparation &

TradeStation® Optimization

Step2 – Detecting the optimal

Strategy Potential/Parameters

Step3 – Detecting the optimal

Strategy Exit Method

Step4 – Detecting the optimal

Strategy Result

Step5 – Walk Forward

Analysis/Optimization (WFA)

Walk Forward Analysis Overview

Walk Forward Analysis Setup Module

Walk Forward Analysis – Filter

Definition (Step1)

Walk Forward Analysis – Sort

Definition (Step2)

Walk Forward Analysis – Defining

the Period Setup/Sequence

Defining a sequence of walk forward

Period setups

Walk Forward Analysis – Check your

Save Result Options

Walk Forward Analysis – Starting

Walk Forward Analysis

Walk Forward Analysis – Treeview

Display

View best WFA Drawdown, Volatility,

ProfitFactor and Robustness

Preparing TradeStation® - Opening

your Strategy Code

Adding the BTWFMgr Data Collection

Section

Sample of Data Collection Section

Detecting the optimal Strategy

Potential/Parameters

Analyzing the Strategy Per Trade

Potential

Analyzing the Strategy Yearly

Potential

Analyzing the Strategy Parameter

Potentials

Analyzing the Strategy Context

Variables

Detecting the optimal Strategy Exit

Method

Analyzing the Strategy Exit Results

Analyzing the Strategy Exit

Parameters

BTWFMgr Configuration and Preferences

Smart Ranking Analysis Settings

Best Trade Permutation Analysis

Settings

Walk Forward Analysis+Optimization

Settings

Strategy Potential &

Probability Analysis Settings

Initial Data Conversion Settings

Position Exit Manager (PEM)

Settings

Introduction to BTWFMgr

Developing

a successful trading strategy is a craft - some might even say an art.

You

will need the right tools to be able to test, evaluate and optimize your

trading strategies.

To

assist you in this task and adventure - we have developed a new powerful

software tool:

”Diamond Backtesting with Walk Forward Manager”

– or in short BTWFMgr.

For more current information and to download go to http://www.ProfSoftware.com/bt

We have grouped the BTWFMgr manual into the following chapters:

·

Overview

Presents the main BTWFMgr functions with a brief description

·

BTWFMgr Basics

Introduces you to some basic concepts of BTWFMgr and

shows you how to get started and some basic BTWFMgr functions

·

Strategy Development

Describes some basic concepts how strategies can be developed (using BTWFMgr)

·

Function Reference

Here we show you each BTWFMgr function in greater detail

·

Licensing & Ordering

Details

about ordering BTWFMgr and licening

·

Installation

Step-by-step

guide how to install BTWFMgr

·

Glossary

Explains

basic terms and abbreviations used in this BTWFMgr manual

We

hope you will find BTWFMgr a valuable tool and invite your feedback at: pss@pobox.com

Check

frequently for updates – as we continuously improve and expand BTWFMgr at:

www.profsoftware.com/bt/dl.htm

BTWFMgr works for example with the TradeStation Open Platform® (TradeStation.com)

and enhances one of the most powerful trading and strategy research

platforms available

which seamlessly integrate the charts and strategy and fully automated

executions.

Overview

Below

we will introduce you to the main functions BTWFMgr is offering you,

so

you can analyze and improve your strategies.

For more details on each function use the Reference Chapter

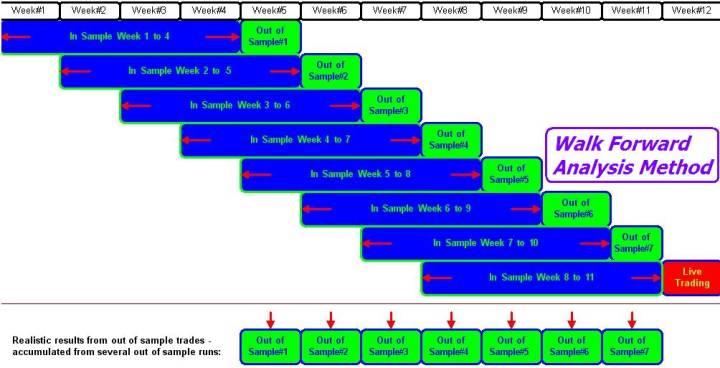

Fully automated advanced Walk Forward Analysis (WFA)

Provides

you with a powerful, more realistic backtesting method, testing essentially the

predictability/robustness, instead of the usual unrealistic curve fitting

optimization,

saving you hours or even days of cumbersome calculations. Below is a 4

week/1week example:

All

aspects of the walk forward analysis can be customized:

Filter, Sort, In/OutSample Sequences/Clusters - using intuitive Filter/Sort and

Period Manager interfaces.

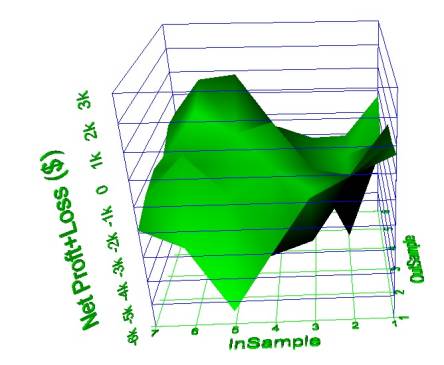

Walk

Forward Analysis Results can be shown even in a 3D cluster view

presenting in this example the correlations between in and out sample

variations:

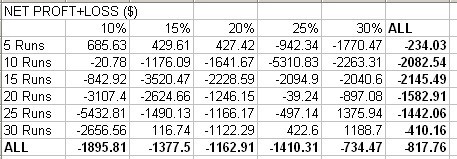

Also

results can be viewed as a spreadsheet/2D view.

Below is an example showing the clusters (using 5 to 30 runs and 10 to 30% out

of sample):

These

Walk forward result views can use any of the many statistics available:

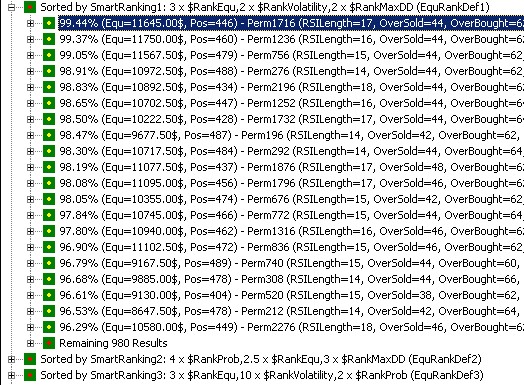

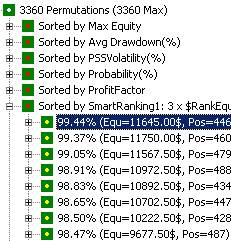

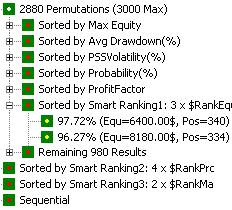

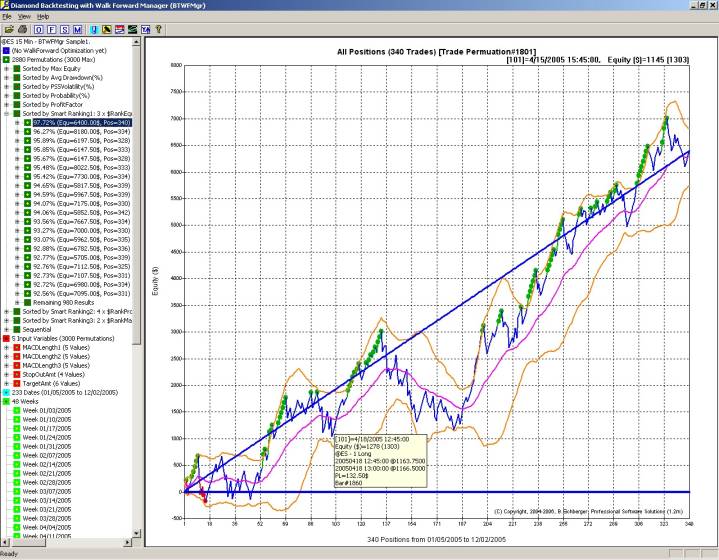

Smart/Hybrid Ranking

Finds

you the best backtesting results by combining your most important

(customizable) sort criteria into a hybrid. Below is an example using

Equity(3x), Volaitility(2x) and Drawdown(2x):

![]()

The ideal result would be at the top in all sort criterias = 100%,

below is an example, showing the smartranbking, with the best hybrid result

(99.44%) on top:

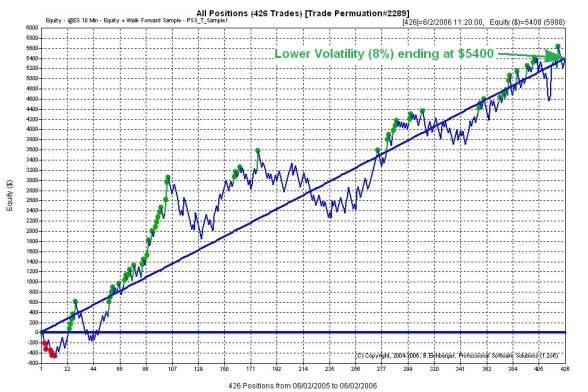

Innovative Volatility Analysis

For

most traders a fairly predictable, smooth equity graph is preferable to

an equity graph with wider swings, but a higher ending equity. The innovative

volatility analysis measures the “swing” around the smooth equity income line.

Below is an example of the fairly smooth equity graph:

below

we see the same ending equity($5400) but a much higher volatility(17%) and

wider “swings”:

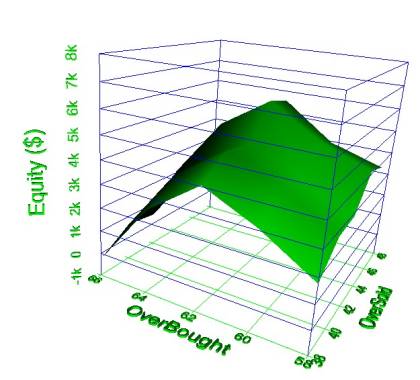

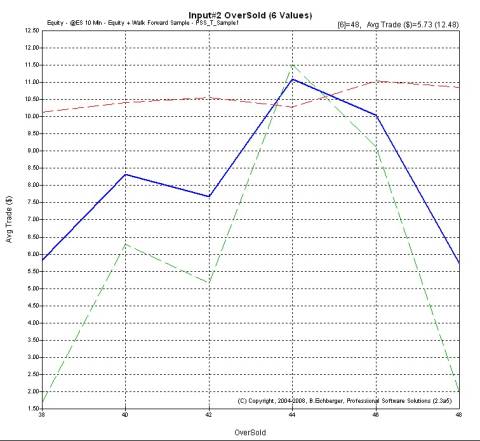

Advanced Strategy Input Parameter Analysis

Shows

you a detailed visual analysis of the effect of EACH strategy input parameter

variations on the overall result, below is an example in 3D view, combining RSI

oversold and overbought parameter:

Also

a 2D graph is available - showing the overall(blue),

long(green) and short(red)

effect of each parameter value on the overall result:

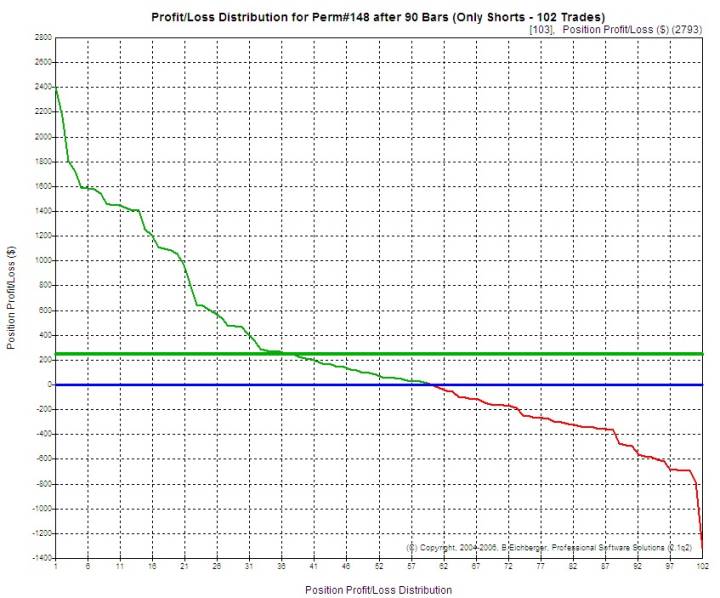

Position Profit/Loss Distribution Analysis

Helps

you detecting misleading outliers in your equity graph:

ranking winners(green) and losers(red) – and showing the overall average line at

$240:

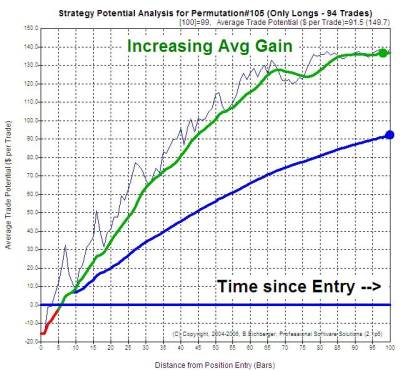

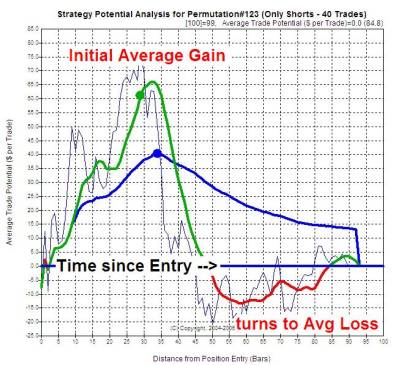

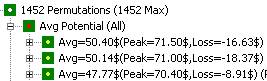

Innovative Trading Strategy Potential Analysis and Optimization

Track

how the market response on average to your entries (Potential Analysis),

helping

you to detect the maximum trading opportunities and finding best entry points,

using

ONLY ENTRY POINTS, before you focus on develop the exit logic in your strategy.

Below is an example of a stable gain:

and

an example of a gain which expires after around 45 bars since entry:

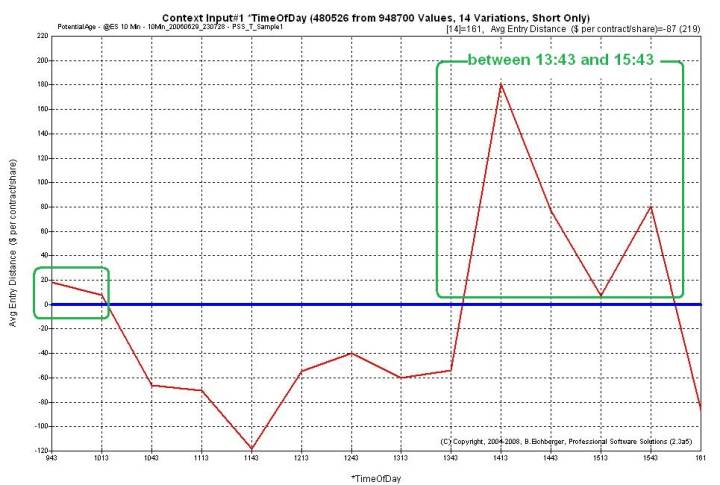

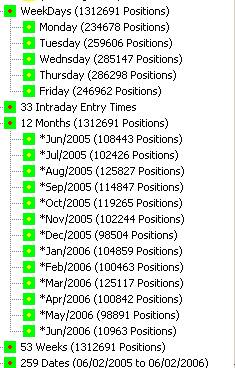

Equity Intraday Time Analysis

Identify

the best intraday trading times of your startegies.

In the “Equity Time Analysis” sample below

we see that 9:43 to 10:13 and 14:13 to 15:43 are the best trading times:

(You

can adjust the time interval in the configuration: Treeview/EquTimeLength - the

default is 30 minutes)

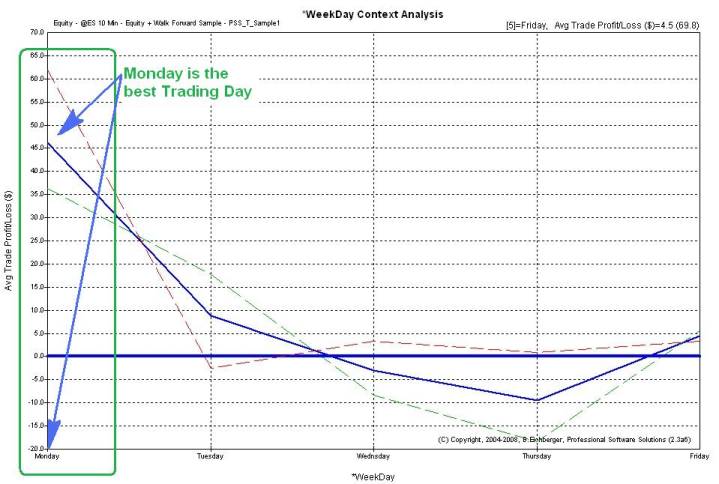

Identify the best Weekdays and Entry Intraday times

This

function allows you identify the best weekday to trade - for all(blue), long(green)

or short(red).

In

the sample below we can see that Monday is the best trading day:

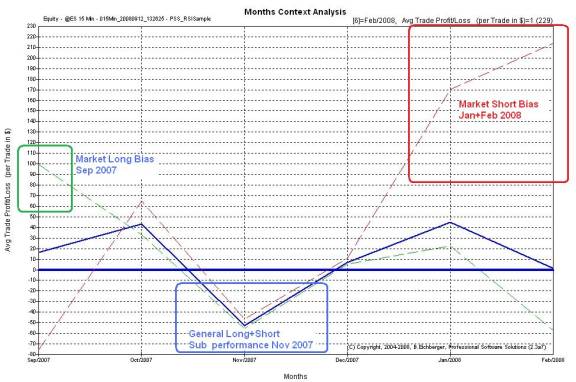

Detect the Market Long/Short Bias

This

function allows you to detect the general long(green)

or short(red) bias (if any)

of your strategy performance. Also periods of strategy sub performances are

shown:

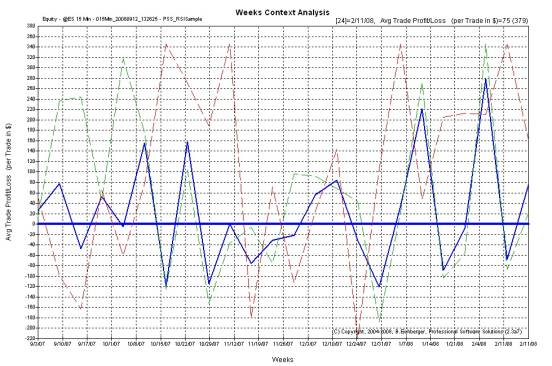

You

can also use a more detailed weekly market long/short bias analysis:

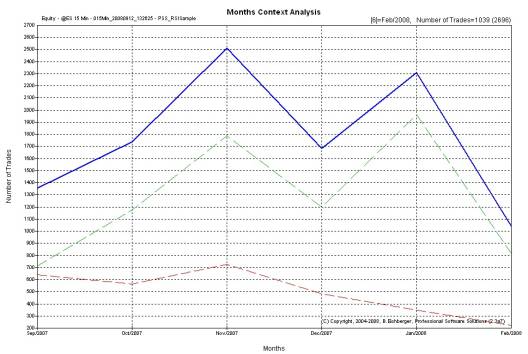

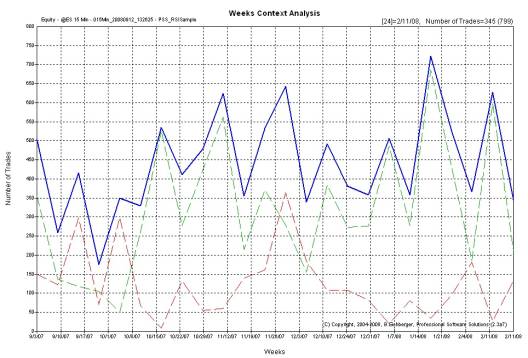

Detect the Strategy Trading Frequency

This

function allows you to detect how frequently your strategy is trading over

time,

separated by long(green), short(red) and total

trades(blue):

You

can also see the more detailed weekly (and even daily) frequency analysis

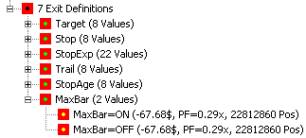

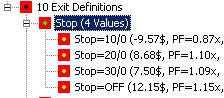

Find the best exit logic - Position Exit Manager (PEM):

After

you have identified the best strategy entries with the best potential, you can

test millions of exit logic variations, using the integrated high speed

(100,000/second) Position Exit Manager (PEM),

to detect the best way to exit. You can use any combination of various exit

functions:

Exponential+Linear

Target, Exponential+Linear StopOut, Trailing, breakeven, age etc.

Below we see a visual example how PEM can manage your positions:

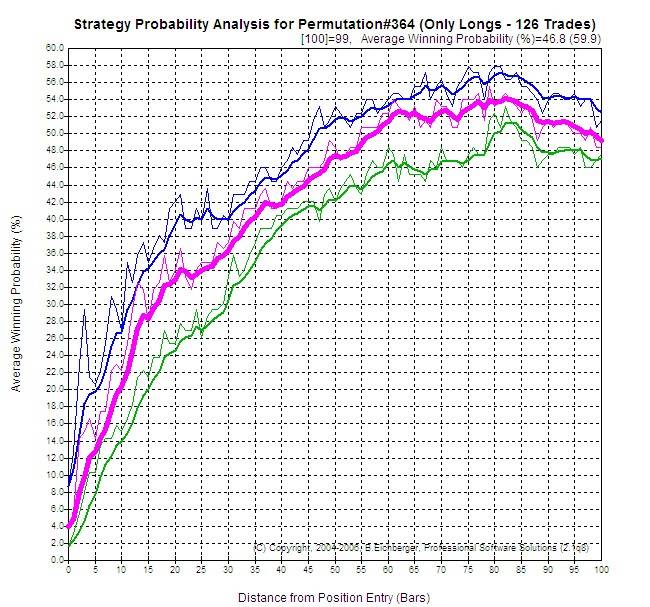

Strategy Probability Map

The

"probability map" function, allows you to detect the best probability

areas,

in the time based market response (Potential) analysis.

Below we can see an the best probability is reached after 75 bars,

for the three (customizable) target levels: $50(green),

$100(magenta), $150(blue):

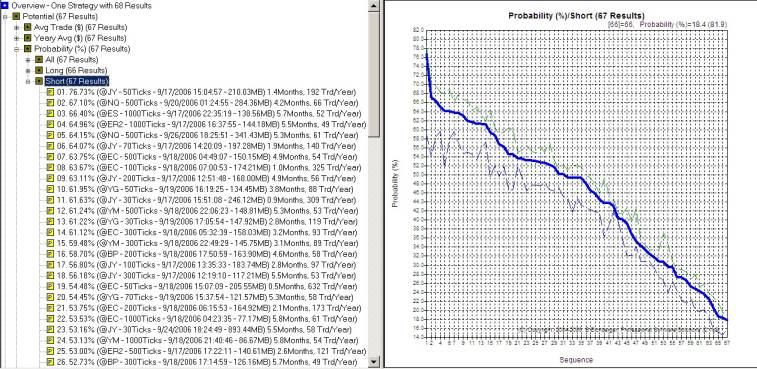

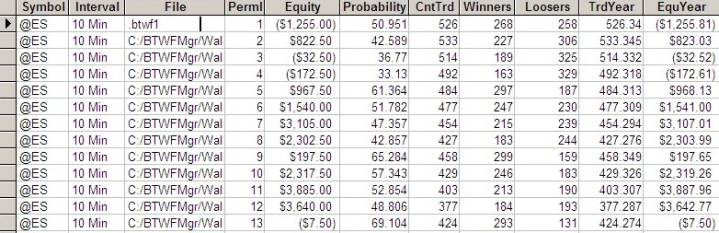

Visual Multi Timeframe/Symbol Analysis - Result Overview Module

After

you have run several backtests for a strategy across symbols and/or timeframes,

you

can quickly detect the best performance using Probability%, Yearly, PerTrdAvg

or PeakAvg$,

calculated

separately by long/short or merged trading,

below

is a screen shot with the best probability results for shorts:

In

the chart three lines are shown:

·

green

thin line = single top result

·

blue

thick line = average of the top 10 results

·

blue

think line = avgerge of the top 100 results

Integrated In depth Performance Analyzer (PerfAna)

This

additional module allows you to perform many in depth equity result operations

and statistics

and also export the trades to a spreadsheet – below is a statistic analysis

view:

You

can merge results from different markets/symbols into one new comprehensive

result/graph

with the Performance Analyzer module.

Export Results to Microsoft Access Database

This

function allows you export the permutation data to a standard microsoft access

database.

Then you can apply any advanced SQL queries and/or reports to process and

detect the best results:

(just

enable the export by setting Setting System/ExportTrdPer to YES and the next

time you open an equity result - all permutations will be exported)

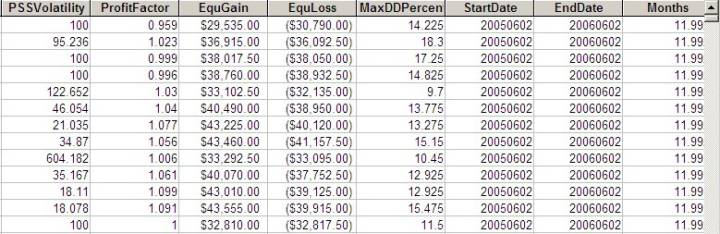

Correlate Context Values with best Potential

You

can add any variable in Potential Mode to the backtesting, so you can detect

any correlation between context variable range(s) and favorable potential

results.

In the example below, we use the angle exponential average (see PSS_RSISample

workspace),

detecting that slightly downward angle (around minus 0.5264) offer the best

returns for shorts(red):

Instant Position Viewing

Provides

you - with a mouse click - with the actual charts of each Position Entry, Exit

and Risk/Reward excursion instantly, so you can evaluate also visually all

entries and their performance - instead of using the cumbersome scrolling in

the charts – in the example below we see:

a) the horizontal blue line (entry price)

b) maximum favorable excursion (green line)

c) maximum unfavorable excursion (red line)

d) Exit price (end of diagonal blue line):

Automated modification of your EasyLanguage Strategy Code

This

function completely automates the preparation of your strategy EasyLanguage

code,

so BTWFMgr can collect all the trades data during the optimization.

(you don't have to be familiar at all with EasyLanguage!)

Below is the interface through which you can modify your strategy code

(PSS_RSISample):

BTWFMgr Basics

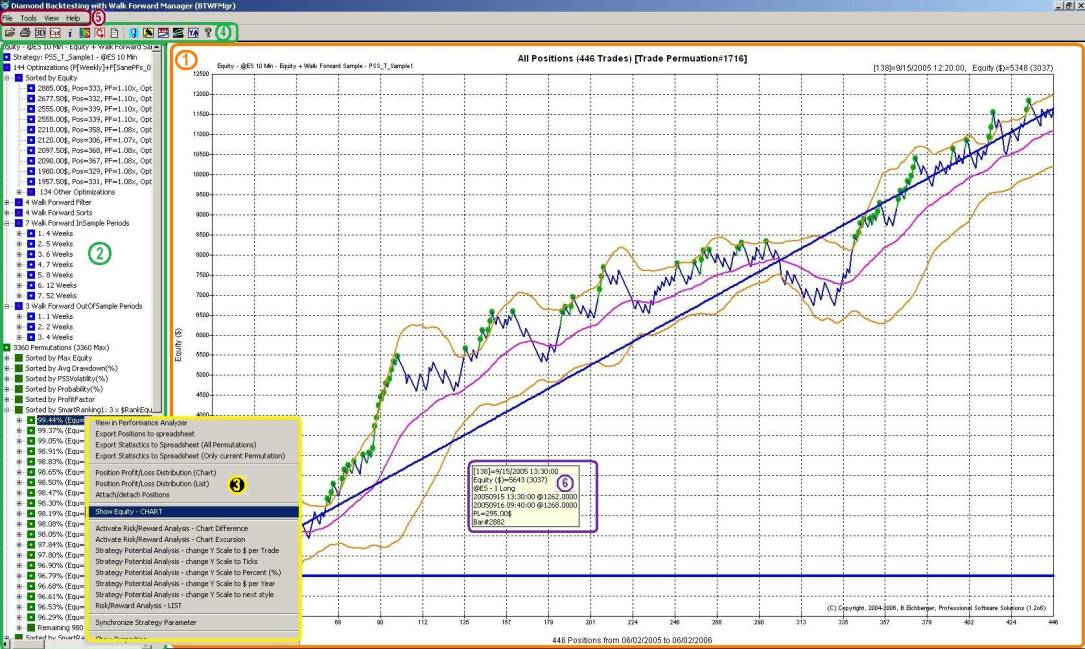

BTWFSMgr Software Layout

BTWFMgr

is using a very visual approach, which (hopefully) makes working with BTWFMgr easy+intuitive.

Similar to the windows explorer, all relevant items are shown in a window on

the left side (treeview),

were can “zoom” in or out any item. The “display”

shows the current details as a chart or even 3D View.

|

Main Display (1) |

shows

the chart, list or 3D view for the current item from the treeview |

|

Treeview Area (2) |

Shows

the items for the current backtest data in “branches” and subbranches. |

|

Pop-up Menu(3) |

The

list of specific functions for the currently selected element/item. |

|

Toolbar(4) |

List

of the main functions – using icons - accessible via one mouse click |

|

Menu(5) |

All

available functions - accessible via the standard Windows menu interface |

|

Tooltip window(6) |

A

small white window popping up when you move the cursor in the main display |

BTWFMgr Operating Modes

BTWFMgr operates in two main modes:

a) Equity/Walk

Forward Mode: entry and exit points are used for an equity graph for each

permutation

b) Potential

Mode: only entry points are used to detect the best market response for each

permutation

When running the optimization, simply

set the “nBTWFMgrExport” strategy parameter to 2(Equ) or 1(Pot).

See “Strategy Preparation” for

details how to prepare your strategy for BTWFMgr.

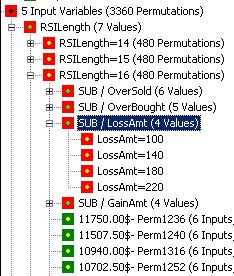

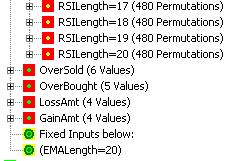

Equity/Walk Forward Mode (nBTWFMgrExport=2)

This is the main mode, were the strategy generates entries AND exits automatically, applying the “Strategy Entry+Exit Logic” for trading decisions. In this “Equity(Equ)” mode, we are optimizing the Equity and overall Strategy results and can run the advanced walk forward analysis, testing predictive-ness.

BTWFMgr comes with an equity sample

“out of the box”, so you instantly can test drive BTWFMgr:

Start/Programs/Diamond

Backtesting/Sample Equity + Walk Forward Analysis

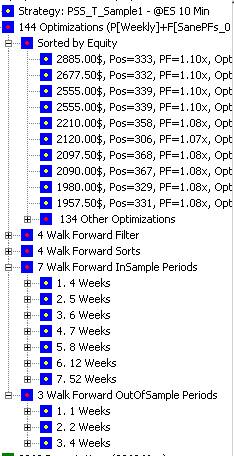

Below are the main Treeview branches

showing the results (more details in further chapters):

|

Title |

|

at the very top showing the symbol,

time frame and the description. In this example: |

|

Walk Forward Optimization

Results |

|

Showing the top 10 Walk Forward

results; Equity total. attached under “134 Other

Optimizations” |

|

Strategy Overall |

|

Showing the overall results or each

permutation. ·

Sorted by Max Equity ·

Sorted by Average Drawdown (%) ·

Sorted by PSSVolatility (%) ·

Sorted by Probability (%) ·

Sorted by ProfitFactor ·

Sorted by SmartRanking1

(Custom Hybrid1) ·

Sorted by SmartRanking2

(Custom Hybrid2) ·

Sorted by SmartRanking3

(Custom Hybrid3) ·

Sorted Permutation Sequence

Number Here you can find out the best

overall results. |

|

Strategy Input Parameter Analysis |

|

In depth Analysis of strategy input

parameter: b) each

individual input parameter c) each

input parameter value d) even

their respective sub values Here you can detect the optimal

parameter range. |

|

Context Parameter Analysis |

|

In this section we track the overall

effect of each |

Potential

Mode (nBTWFMgrExport=1)

This is the initial mode in your

strategy development – only the “Strategy Entry Logic” is used -

which creates the entry points (buy/short) – the exit logic is not yet used.

BTWFMgr analyzes for you how the market

responded – on average – to each series of entries -

generated by each input parameter permutation. This response is shown in the “Strategy

Potential Graph” – allowing you to see how far your strategy potential

moved and how long the move lasted.

BTWFMgr comes with an potential sample

“out of the box”, so you instantly can test drive BTWFMgr:

Start/Programs/Diamond Backtesting

…(BTWFMgr)/ Sample_Strategy_Potential_Analysis

Below are the main Treeview branches

showing the results (more details in further chapters):

|

Title |

|

Shows the details of the backtesting

data: |

|

Exit Optimization Results |

|

Showing the top 10 exit optimization

results |

|

Exit Parameter Analysis |

|

This section shows you the effect of

each exit logic element on the overall result. |

|

Strategy Potential Analysis |

|

This section allows you to find the

best strategy potential and also the extend and duration of the market

response on average(potential). The strategy potential for each

permutation in the backtest is shown and |

|

Strategy Input Parameter

Analysis |

|

This section allows you to track the

effect of each strategy input parameter on the potential and detect the

optimal parameter range. |

|

Strategy Context Variables Analysis |

|

Here you can detect if certain ranges

of additional context variables can filter out adverse results and improve

the performance, Example: |

Data Collection turned off (nBTWFMgrExport=0)

To turn of the data collection OFF, simply

set nBTWFMgrExport to 0 in the strategy before running the backtest

optimization. This might be useful when for example the BTWFMgr trial period

has expired.

BTWFMgr Location+Files

By

default BTWFMgr is installed to the C: drive into the C:/BTWFMgr folder.

All sub folders are created underneath this BTWFMgr “home” directory.

Each strategy has its own sub folder, with another subfolder for each symbol:

Example: C:\BTWFMgr\PSS_RSISample\@ES

Each backtest generates its own data files:

Examples:

C:\BTWFMgr\PSS_RSISample\@ES\015Min_20080912_132625.btwf1+2 (Equity data)

C:\BTWFMgr\PSS_RSISample\@ES\P_015Min_20081110_135126.btwf1+2 (Potential data)

{Result} is used below for the basic folder and

name of a backtest result - Example:

C:\BTWFMgr\PSS_RSISample\@ES\P_015Min_20081110_135126

Basic BTWFMGR files

Each

backtest generates the following files:

a)

BTWFMgr

Backtesting Definition File (btwf1)

contains general backtest information

b)

BTWFMgr

Backtesting Event Data File (btwf2)

contains the raw trading events, like buy/sell

c)

BTWFMgr

Backtesting Position Data File (btwf3)

contains the compacted trading information derived from the btwf2 file

d)

BTWFMgr

top results File ({Result}-Best.CSV)

contains the result overview as a small spreadsheet,

which is used by the BTWFMgr overview module

to compare the various markets and timeframe results

BTWFMgr additional Files

In addition the

following files are generated by various functions:

·

BTWFMgr

Result Distribution File ({Result}-Equ.CSV)

Listing all permutations for the selected sort criteria

·

BTWFMgr

Permutation Database ({Result}.MDB)

Exporting the statistics for each permutation to a Microsoft access database

for further processing

and even advanced SQL queries on your results

·

BTWFMgr

“long only” Position Data File ({Result}-L.btwf3)

Extracted all the long positions from the {Result},

to identify the best results for the long side

·

BTWFMgr

“short only” Position Data File ({Result}-S.btwf3)

Extracted all the short positions from the {Result}m

to identify the best results for the short

side

BTWFMgr Walk Forward Files

The Walk Forward

Analysis(WFA) generates its own folder and files within/underneath it:

·

BTWFMgr

Backtesting WFA Data File (btwf4)

contains the details of the Walk Forward Analysis(WFA)

Example: {Result}\P[Daily]+F[PFCheck3]+S[SortMix1].btwf4

·

BTWFMgr

Backtesting WFA equity overview File (CSV)

contains the WFA results sorted by ending OSA equity:

Example: {Result}\P[Daily]+F[PFCheck3]+S[SortMix1].csv

·

BTWFMgr

Backtesting WFA Result overview File (-Results.CSV)

contains the details for each WFA result:

Example: {Result}\P[Daily]+F[PFCheck3]+S[SortMix1]-Results.csv

·

BTWFMgr

WFA log files (CSV)

contains the various log file for each Walk Forward Analysis(WFA).

A new subfolder is generated:

Example: {Result}\P[Daily]+F[PFCheck3]+S[SortMix1]\XXX

A

special process allows you to migrate the BTWFMgr “home” directory to another

drive

(see

the “General/DRIVE” Configuration setting).

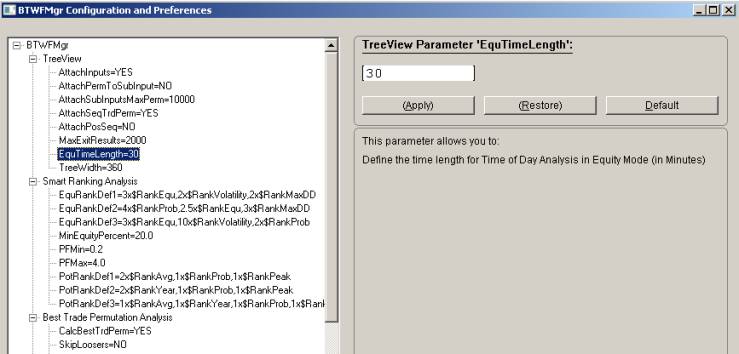

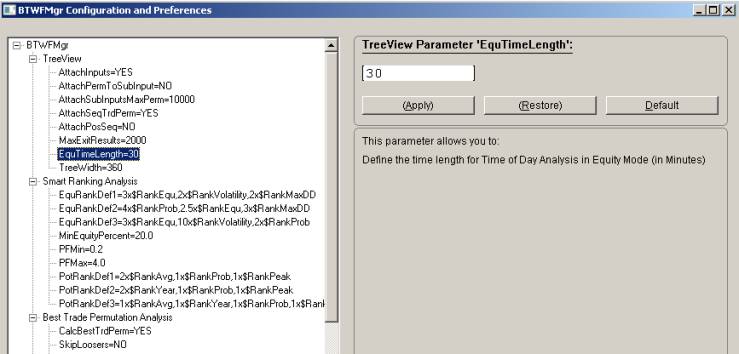

BTWFMgr Configuration and Preferences

BTWFMgr allows you to easily change

almost all of its internal parameters,

so you can tailor the behavior to your needs.

To start the configuration, simply click on the ![]() icon

in the toolbar –or- Ctrl+C –or-

icon

in the toolbar –or- Ctrl+C –or-

select or from the in the Menu: File/Backtesting Configuration and Preferences

(Ctrl+C)

All parameters are organized by topics:

·

TreeView

·

Smart Ranking Analysis

·

Best Trade Permutation Analysis

·

Walk Forward Optimization

·

Strategy Potential & Probability

Analysis

·

Initial Data Conversion

·

Position Exit Manager (PEM)

·

General

·

Chart

Below each topic the associated

parameters are attached. You can expand and collapse each topic,

by clicking on the plus or minus mark (![]() and

and ![]() ) in front of the topic.

) in front of the topic.

To see a more detailed description -

click on the parameter,

and the right window section will show the description and current setting -

You can now:

·

Change the parameter value (simply

enter/select the new value and click on “Apply”)

·

Restore to the previous setting – after

an erroneous change for example – click on “Restore”

·

Switch to the parameter default value –

click on “Default”

Close the Configuration Window via the

“Close” button, the ESC key or the ![]() window button.

window button.

The new parameter settings is shown

with a star and activated next time you open BTWFMgr again.

A detailed description of each parameter is below in the “reference section”.

Below is a sample screen of the BTWFMgr Configuration and Preference Window:

(You can also edit the configuration parameters directly in the

C:/BTWFMgr/BTWFMgr.ini file)

BTWFMgr Toolbar

BTWFMgr

offers many functions directly from the toolbar:

![]()

Below is a list of each function available from the toolbar:

|

ICON |

Shortcut |

Description |

|

|

Ctrl+O

|

Open

a new BTWFMgr data file (btwf1) |

|

|

File/Print |

Print

current view |

|

|

Ctrl+3 |

Shows

Results in 3D View |

|

|

Ctrl+R |

Runs

the Walk Forward Analysis(WFA) in Equity Mode |

|

|

Function/Show

Data Properties |

Shows

the properties for the current data set |

|

|

Function/Split

into Long/Short |

Creates

new data sets for longs/shorts only |

|

|

Function/Recalculate

data set |

Recalculates

the current data set with changed parameters |

|

|

Function/Result

Distribution |

Activates

the Result Distribution function |

|

|

Function/Create

Overview |

Activates

the BTWFMgr overview module to |

|

|

Function/Prepare

your strategy |

Activates

the module to prepare your strategy for BTWFMgr |

|

|

Function/Configuration

and Preferences |

Set

Configuration and Preference parameter |

|

|

|

Switch

between Equity and Draw Down Chart Style |

|

|

|

Switch

Bollinger Band Display on/off |

|

|

|

Change

the Y Scale display to the next available style |

|

|

Help |

Activate

the BTWFMgr Help Module + License Manager |

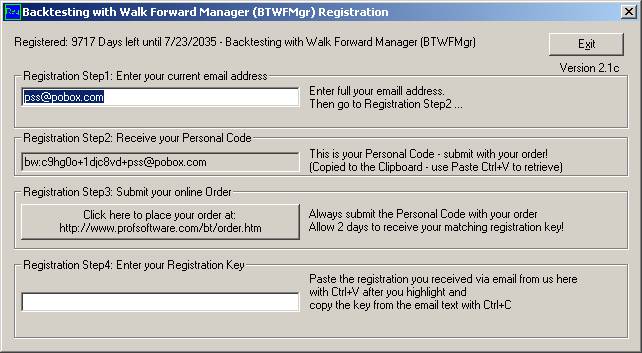

BTWFMgr Licensing

BTWFMgr

comes with a free 15 days trial period – offering full functionality.

Check your BTWFMgr license status via: Help/BTWFMgr License Manager –or-

Start/Programs/Diamond Backtesting …/License Manager

After the trail period expires - order your BTWFMgr subscription online at:

http://www.profsoftware.com/bt/order.htm

BTWFMgr

is available at a minimal cost in convenient 3, 6, 12 and 24 month

subscriptions or unlimited.

We offer discounts for longer subscriptions and grouping orders together for

other users or computers.

Over the long run the most economical is the outright/unlimited mode.

Each BTWFMgr license is on a per computer basis and not transferable.

You can request a trial extension – send us via email us the personal code:

Example: bw:c9hg0o+1djc8vd+pss@pobox.com

During the trial period - you have 10 free data conversions available.

Before the next of the 10 conversions is used up - a confirm box will appear:

click YES to use the next of the 10

trail data conversions - otherwise click NO.

Machine Replacement or Upgrade

While

BTWFMgr registration keys are purchased specifically for a single computer, PSS

may, at our discretion, allow you to transfer a serial number to a new or

upgraded computer. Such transfers will not be allowed at a rate of more than

once per 6-month period, and proof of ownership of a new or upgraded computer

(such as an invoice or receipt) will be required along with a signed statement

requesting the transfer. Contact us at pss@pobox.com if you would like to

request a BTWFMgr license. This transfer option does not in any way alter or

override the End User License Agreement (EULA) stating that a registration key

is purchased for one machine only.

Strategy Development

Below

we are presenting to you briefly the key concepts used in the BTWFMgr.

In few basic steps we show you how to quickly develop and test your strategy

with BTWFMgr.

Each Trading Strategy has two major elements:

·

Strategy Entry Logic – when to enter a position (buy/short)

·

Strategy Exit Logic – when to exit/reverse a position (sell/cover)

Strategy development starts in most cases with defining just the entry

condition(s) and then

translating those rules into the ”Strategy Entry Logic“ (i.e.

EasyLanguage® from TradeStation®).

BTWFMgr

allows you to optimize initially only the entry logic, without any exit logic

yet,

so you can identify initially the best entry points which yield the best “Strategy

Potential” (see below).

Once

the best “Strategy Potential” has been identified you can then move on

to the other “wing”

of

your strategy, which defines the most profitable way to exit the entries: the ”Strategy

Exit Logic“.

Only

when both “wings” of your strategy – entry AND exit - are independently strong

and healthy,

can your strategy “take flight” and can give you consistent profitable results.

BTWFMgr,

unlike all other backtesting software tools, does not force you to prematurely

include the exit logic, but allows you to first test only the entry logic

(Potential Mode) and then later

the entry AND exit (Equity Mode), so you can optimize each element

individually.

BTWFMgr

is collecting its backtesting data in the background while the Backtesting Optimization

is processing the data (designed to work currently with the TradeStation®)

8.X platform).

When the backtest process completes, BTWFMgr is automatically activated, and

will immediately convert and analyze and save the collected data, and then

present to you the results in several interactive graph,

so you can quickly identify the best results and apply the various functions to

analyze the results.

Step1 – Strategy Preparation & TradeStation® Optimization

In

the quick strategy preparation – we will add a small section at the end of your

strategy code,

which will perform the data collection in the background for you. BTWFMgr can

do this one time modification of your strategy automatically, so you do not

have to be an EasyLanguage expert!

(More

details below in the “Strategy Preparation” chapter)

Step2 – Detecting the optimal Strategy Potential/Parameters

The

only reason for your strategy to enter a new position (buy/short) at the

various entry points, is,

that you expect – on average – that the market will move in the anticipated

direction, allowing you to realize a profit. This assumption can now be

precisely tested and verified using BTWFMgr’s

powerful and innovative approach – detecting the best Trading

Strategy Potential.

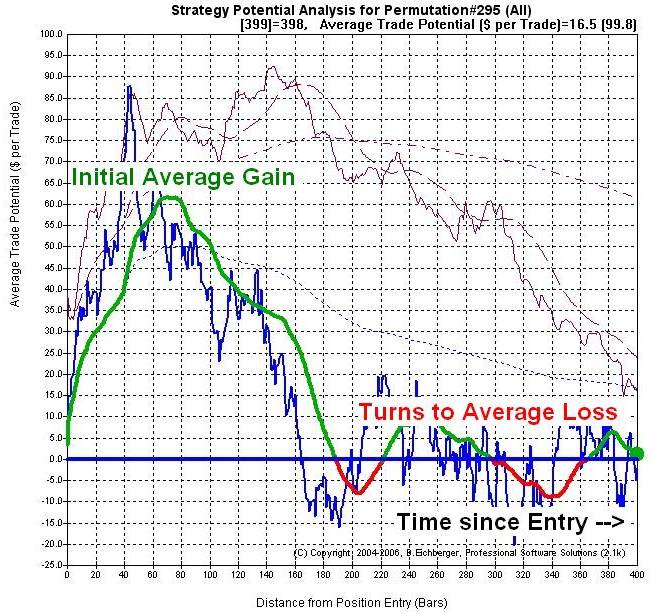

Lets look at one example:

In this example the market moves initially in the

anticipated direction (green line) and reaches after 60 bars and average gain

of $60 (on each trade). Then the market moves – on average - against you.

The “Strategy Potential Graph” shows you clearly:

- How much maximum profit you can expect (highest point of green line)

- When that maximum profit is reached

- How the strategy potential develops over time and if the market turns against you.

- Calculates also a separate Potential for longs and shorts only

- Show the optimal ranges for each strategy input parameter

BTWFMgr is calculating – for each strategy input permutation – the most best and worst strategy potential excursion and then presenting you a list of the best results.

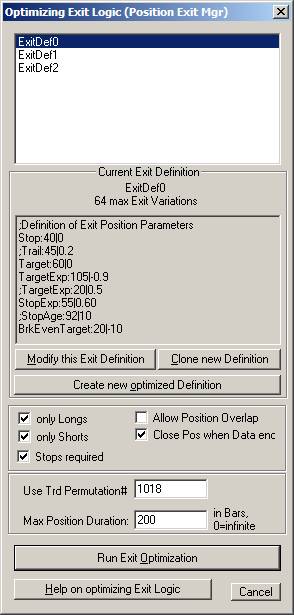

Step3 – Detecting the optimal Strategy Exit Method

Initially the optimal “Strategy Exit Logic” method is

not yet known, only the “Strategy Entry Logic”.

After we have identified the best strategy profit potentials, we can now detect

the best exit methods.

BTWFMgr come with an integrated “Position Exit Manager

(PEM)” which can evaluate 100,000 different exit method variations per

second, once all variations are tested BTWFMgr will then show you a list with

the best results. Then you can add the corresponding ”Strategy Exit Logic“

to your strategy.

In Potential Mode click on the OPT toolbar button and then initially create a

default Exit Definition:

Click on “Create Exit Definition”. You can then “Modify Exit Definition” or

directly “Run Exit Optimization”.

Step4 – Detecting the optimal Strategy Result

Now

with both the exit and entry logic - you are ready to re-run the TradeStation®

Optimization.

Set the nBTWFMGrExport strategy input parameter to 2 (Strategy Equity mode).

BTWFMgr will show you the best results

in several different lists:

·

Sorted by Max Equity

·

Sorted by Drawdown(%)

·

Sorted by PSSVolatility(%)

·

Sorted by Probability(%)

·

Sorted by ProfitFactor

·

Sorted by Smart Ranking1 – a custom

hybrid of above elements

·

Sorted by Smart Ranking2 – a custom

hybrid of above elements

·

Sorted by Smart Ranking3 – a custom

hybrid of above elements

BTWFMgr also shows you the optimal

ranges for each strategy input parameter and even

individual results for each specific strategy input parameter value!

Step5 – Walk Forward Analysis/Optimization (WFA)

In

this final step – to verify also using the powerful Walk Forward backtesting

method,

that your strategy has a realistic profit potential.

In many cases the curve fitted (fantastic) results in step4 are not likely to

repeat,

Which

leads usually to costly and discouraging trading results.

The new “Walk Forward backtesting method” can give you a much more

realistic preview and test of the true results your strategy can produce.

BTWFMgr

allows you to:

·

Use

any filter formula you devise

·

Use

any sort formula you want to test

·

Sort

all walk forward results identifying the best filter and sort method

·

Use

any in-sample and out-of-sample period setup

·

See

the out-of-sample results in one comprehensive equity graph or spreadsheet or

even 3D View

·

Show

the last period input parameter – which are then used in the actual live

trading

See

more information in a separate chapter “Walk Forward Analysis(WFA)” below.

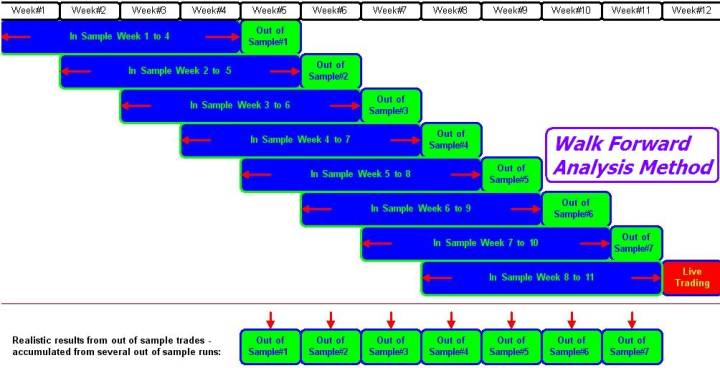

Walk Forward Analysis (WFA)

BTWFMgr

contains also the advanced Walk Forward Analysis (WFA), which allows you

essentially to “fire-test” your strategy performance, using historical data,

and to find the most robust and predictive approach and parameters. Walk

Forward Analysis (WFA) is available in BTWFMgr Equity mode.

Walk Forward Analysis Overview

Walk

Forward Analysis (WFA) is a powerful automated process – saving you hours or

days of manual error-prone calculations. The following WFA steps are performed:

·

Identify

the customizable “In-Sample” period (blue section below)

·

Extract

all candidates from the “In-Sample” period using the WFA Filter and

eliminate all undesired results. In some case ALL candidates are eliminated.

·

Find

the “best” “In-Sample” permutation based on your WFA Sort specifications

·

Shift

the focus to the next customizable “Out-of-sample” period (green sections

below)

which follows directly the “In-Sample” period

·

Apply

this “best” permutation to the “Out-of-sample” period,

thereby “fire-testing” and checking if the “In-Sample” performance actually

continued.

·

Append

this “Out-of-sample” result to the overall WFA result.

·

Move

to the next “In-Sample” period until all data has been processed.

·

Show

the “best” strategy parameter for the future period (next “Out-of-sample”

period) (red below)

This WFA approach avoids the usual costly “curve-fitting” phenomenon, when a

stellar performance, does in many case NOT continue in the future live trading!

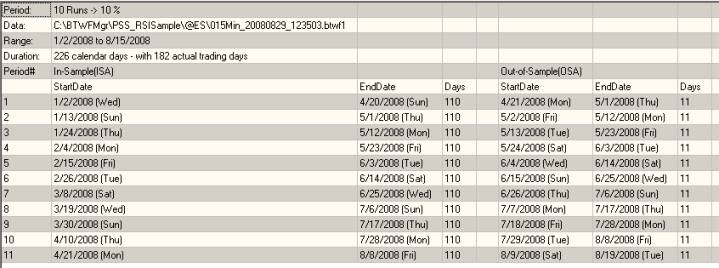

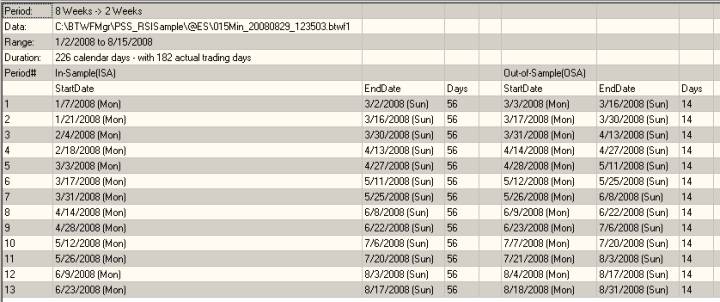

Below is an example using a 4 week “In-Sample” period and one week

“Out-of-sample” period

with 7 walk forward steps:

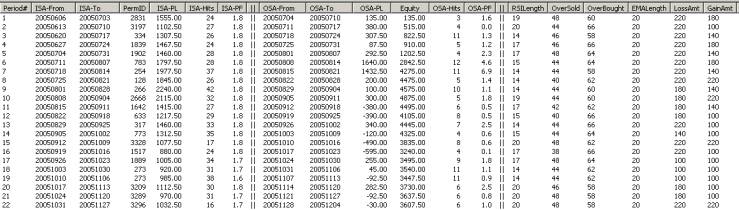

Below

is a BTWFMgr example of a 4 week “In-Sample” period and one week

“Out-of-sample” period:

(WFA Optimization#3 of the WalkFwd.btwf1 sample data set)

|

Column |

Example |

Description |

|

Period# |

1 |

Walk

Forward period, starting at 1 |

|

ISA-From |

20050606 |

“In-Sample”

starting date (Jun 6th, 2005) |

|

ISA-To |

20050703 |

“In-Sample”

ending date (Jul 3rd, 2005) |

|

PermID |

2831 |

“Best”

permutation ID for this ISA period |

|

ISA-PL |

$1555.00 |

Profit/Loss

within the “In-Sample” period (using PermID 2831) |

|

ISA-Hits |

24 |

Number

of positions the “In-Sample” period |

|

ISA-PF |

1.8 |

ProfitFactor

within the “In-Sample” period |

|

|

|

|

|

OSA-From |

20050704 |

“Out-of-Sample”

starting date (Jul 4th, 2005) |

|

OSA-To |

20050710 |

“Out-of-Sample”

ending date (Jul 10th, 2005) |

|

OSA-PL |

$135.00 |

“Out-of-Sample”

profit/loss within current period |

|

Equity |

$135.00 |

Overall

OSA equity total |

|

OSA-Hits |

3 |

Number

of positions the “Out-of-Sample” period |

|

OSA-PF |

1.6 |

ProfitFactor

within the “Out-of-Sample” period |

|

|

|

|

|

RSILength |

19 |

Strategy

Parameters representing the ”best” Permutation ID 2831 |

After the Walk Forward Analysis (WFA) you can then use the WFA Cluster Analysis

and 3D View to detect the best WFA trading parameters (more details below):

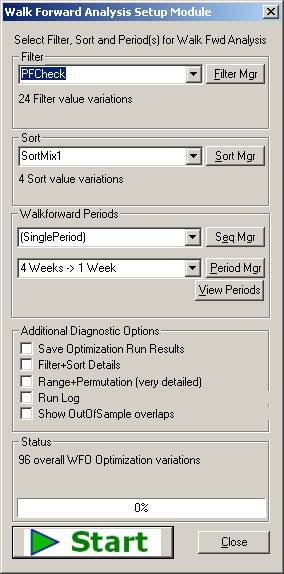

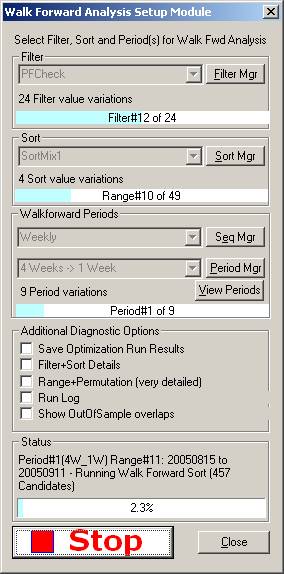

Walk Forward Analysis Setup Module

First

load the Equity result you would like to work with or click File/Open

WalkForward Sample File.

To activate the WFA Module:

·

click

on the ![]() (Optimize)

icon in the toolbar –or-

(Optimize)

icon in the toolbar –or-

·

Ctrl+R

–or-

·

select

from the menu: Functions/Run Optimization (Ctrl+R)

Follow

the simple steps below to run your Walk Forward Analysis(WFA) (explained in more details below):

·

Select/Define

your WFA Filter

·

Select/Define

your WFA Sort

·

Select/Define

your WFA Period Setup

·

Select

any “Additional Diagnostic Options” – usually all are unchecked for faster

performance

·

Click

on the ![]() button and confirm

button and confirm

·

Wait

for the WFA to complete – BTWFMgr shows you the overall and individual progress

in %

·

While

WFA is running you can click on the ![]() button to pause or

abort.

button to pause or

abort.

to continue the WFA press the ![]() button

button

·

When

WFA has completed BTWFMgr will prompt you and

display the new WFA result branch in the treeview.

Below you can see the Walk Forward Setup module:

Walk Forward Analysis – Filter Definition (Step1)

The

first step in the Walk forward Analysis(WFA), is to eliminate unwanted candidates

from the complete list of all trade permutations within each “In-Sample” range.

This process is repeated for each WFA period.

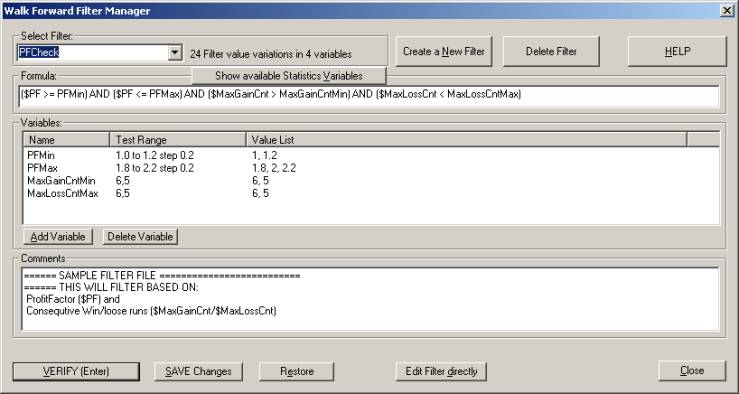

Select the Filter to be used in the WFA from the list of Filters in the Walk

Forward Setup module:

With the “Filter

Manager” you can create and manage your own filter(s).

You

can also select “NoFilter” from the list – if you do NOT want to filter any

permutations.

Filter Manager

BTWFMgr

contains the easy “Filter Manager” interface– assisting you in creating/modifying

your WFA filters.

Simply click on the ![]() button in the Walk Forward

Setup module to activate the “Filter Manager:

button in the Walk Forward

Setup module to activate the “Filter Manager:

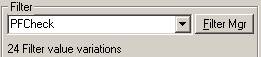

BTWFMgr

will show the number of filter variations next to the selected Filter:

”24 Filter variations in 4 variables”

which is the product of: 2xPFMin, 3xPFMax,2x MaxGainCntMin, 2x MaxLossCntMin.

Filter Formula

BTWFMgr

allows you to specify a formula, a simple logical expression, with a TRUE/FALSE

result.

TRUE=keep the permutation as a candidate, FALSE=discard the permutation in this

“In-Sample” range.

Below is a simple formula, which tests if the ProfitFactor ($PF) is at or above

1.0 (breakeven point):

($PF >= 1.0)

In

other words, we discard any permutations with a ProfitFactor below 1.0 (total

loss > total gains).

BTWFMgr

allows you even to go one step further and introduce “filter variables”, so you

can test several different filter variable values and determine which value(s)

yield the best overall results.

In the example below we replace the fixed “1.0” value with a new “PFMin”

variable (case sensitive):

($PF >= PFMin)

BTWFMgr allows you to define the values for “PFMin”:

PFMin=0.9 to 1.3 step 0.1

BTWFMgr

will run 5 tests with the following “PFMin” values:

0.9, 1.0, 1.1, 1.2, 1.3 (0.9 and 1.3 in 0.1 steps)

To see a list of available “Filter Statistics Variables” click on ![]()

or select from the list below:

Filter System Variables

Below

is a table of all system variables available for the Filter and Sort Formula:

|

$Equ |

Ending Equity |

|

$CntGain |

Number of Winning Trades |

|

$CntLoss |

Number of Losing Trades |

|

$CntTrd |

Number of all Trades |

|

$GrossGain |

Total of all Gains |

|

$GrossLoss |

Total of all Losses |

|

$AvgGainAmt |

Average Winner Amount |

|

$AvgLossAmt |

Average Loser Amount |

|

$MaxGainAmt |

Max Winner Amount |

|

$MaxLossAmt |

Max Loser Amount |

|

$MaxGainCnt |

Max Winner in a row |

|

$MaxLossCnt |

Max Losers in a row |

|

$PF |

ProfitFactor ($GrossGain / $GrossLoss) |

|

$PFAvg |

ProfitFactor ($AvgGainAmt / $AvgLossAmt) |

|

$Prob |

Probability(%)$CntGain/$CntTrd |

|

$MaxDDAmt |

Max Drawdown Amount (negative) |

|

$MaxDDPer |

Max Drawdown (% of Starting Capital) |

|

$DDAvg |

Drawdown average (% of ending Equiy) |

|

$StdDevAmt |

Standard Deviation Amount of all Trades

Profit/Losses Amounts |

|

$StdDevPer |

Standard Deviation (% of Starting

Capital) |

|

$VolatilityAmt |

Volatility

Amount = Avg distance$ from straight Income line |

|

$VolatilityNet |

Volatility

(% of Starting Capital) |

|

|

|

|

$RankEqu |

Equity Rank (100%=best/highest,

0%=worst/lowest) |

|

$RankMaxDD |

Drawdown Rank (100%=best/smallest,

0%=lowest/highest) |

|

$RankVolatility |

Volatility Rank (100%=best/smallest,

0%=lowest/highest) |

|

$RankProb |

Probability Rank (100%=best/highest,

0%=worst/lowest) |

|

$RankPFGross |

ProfitFactor ($PF) Rank

(100%=best/highest, 0%=worst/lowest) |

|

$RankCombo1 |

Smart Ranking Result1(%)

(100%=best/highest, 0%=worst/lowest) |

|

$RankCombo2 |

Smart Ranking Result2(%)

(100%=best/highest, 0%=worst/lowest) |

|

$RankCombo3 |

Smart Ranking Result3(%)

(100%=best/highest, 0%=worst/lowest) |

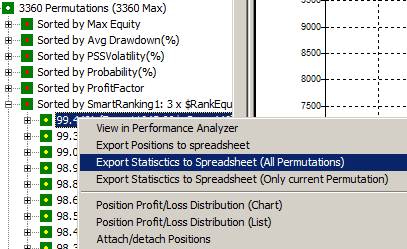

To

check the ranges and see actual values for each of these system variables,

right click on any permutation

in the treeview and select “Export Statistics to Spreadsheet (All

Permutations)“.

Filter Math Functions

BTWFMgr

offers even the use of math functions in your WFA Filter formula, here is the

“PROM: filter formula:

(($AvgGainAmt*($CntGain-sqrt($CntGain)))/($AvgLossAmt*($CntLoss-sqrt($CntLoss))))>

PROMMin

Below is a table of available math function in the WFA Filter Formula:

|

abs(x) |

Absolute Value: abs(-5) = 5 |

|

foor(x) |

largest integer that is less than or

equal to x: floor(2.8)=2, floor(-2.8)=3 |

|

sqrt(x) |

Square root(x) |

|

sign(x) |

Sign: sign(-3)=-1, sign(0)=0, sign(6)=+1 |

|

exp(x) |

Exponential: exp( 2.302585 ) = 10.000000 |

|

pow(x,y) |

Power of: pow(2,3) =8.00000000 |

|

ln(x) |

Natural

logarithms: ln(9000) = 9.104980 |

|

log(x) |

Decimal

logarithms: log(9000) = 3.954243 |

|

log2(x) |

Binary logarithms : log2(4) = 2.000 |

|

sin(x) |

Sinus:

sin(1.570796) = 1.000000 |

|

cos(x) |

Cosinus: cos(1.570796) = 0.000000 |

|

cmple(x,y) |

Compare if less or equal: cmple(2,3)=1, cmple(2,2)=1, cmple(2,1)=0 |

|

cmplt(x,y) |

Compare if less: cmplt(2,3)=1, cmplt(2,2)=0,

cmplt(2,1)=0 |

|

cmpge(x,y) |

Compare if greater or equal:

cmpge(2,3)=0, cmple(2,2)=1, cmple(2,1)=1 |

|

cmpgt(x,y) |

Compare if greater: cmpgt(2,3)=0,

cmpgt(2,2)=0, cmple(2,1)=1 |

Creating a new Filter

To

create a new filter click on “Create a New Filter”:

·

Choose

if you want to clone the current filter or

create a blank new filter

·

Enter

the new formula

·

Click

on ![]() to see available

statistics variables.

to see available

statistics variables.

·

If

you are using variables - click on “Add Variable”

·

Enter

the new variable name

·

A

new variable with a single “0” value will be added

·

Click

on the “0” value in the “Test Range” column

·

BTWFMgr

will switch to edit cell mode

·

Enter

the new list of values, you have two formats available:

1.0 to 2.0 step 0.2 -or-

1, 1.3, 1.5, 2

·

When

you have added all variables and the formula click on “VERIFY”

·

Enter

any comment or description for the new filter

·

Correct

any errors

·

Finally

click on “SAVE” to actually save the new filter to the file

·

From

now on the new Filter will appear in the pull down menu.

·

If

you want to view the actual filter file content – click on “Edit Filter

directly”

Deleting an exiting Filter

Select

the filter to be deleted and click on “Delete Filter” – confirm the deleting.

Filter File Format

BTWFMgr

stores each WFA filter in a separate text file.

Here is an example of the “PFCheck:” filter file – located at

C:/BTWFMgr/PFCheck.btwff”:

Formula=($PF >= PFMin)

AND ($PF <= PFMax) AND ($MaxGainCnt > MaxGainCntMin) AND ($MaxLossCnt

< MaxLossCntMax)

PFMin=1.0 to 1.2

step 0.2

PFMax=1.8 to 2.2

step 0.2

MaxGainCntMin=6,5

MaxLossCntMax=6,5

;====== SAMPLE

FILTER FILE ==========================

;====== THIS

WILL FILTER BASED ON:

; ProfitFactor

($PF) and

; Consequtive

Win/lose runs ($MaxGainCnt/$MaxLossCnt)

The first line is always the Formula

Formula=($PF

>= PFMin) AND ($PF <= PFMax) AND ($MaxGainCnt > MaxGainCntMin) AND

($MaxLossCnt < MaxLossCntMax)

Then follow all the Filter Variables with their ranges

PFMin=1.0 to 1.2 step 0.2

PFMax=1.8 to 2.2

step 0.2

MaxGainCntMin=6,5

MaxLossCntMax=6,5

At the end is your description/comment – always starting with a semicolon:

;====== SAMPLE FILTER FILE

==========================

;====== THIS

WILL FILTER BASED ON:

; ProfitFactor

($PF) and

; Consequtive

Win/lose runs ($MaxGainCnt/$MaxLossCnt)

If

you are confident enough you could directly create and edit these filter file

(C:/BTWFMgr/*.btwff)

Walk Forward Analysis – Sort Definition (Step2)

After

the WFA has selected all viable candidates and discarded the rest in the Filter

Step1,

We

still have usually many candidates left.

In this WFA sorting step, BTWFMgr will re-arrange the candidates in a

customizable sort order.

The permutation/candidate showing up at the TOP is the ONE winner,

which is then used in for the “Out-of –sample” calculation.

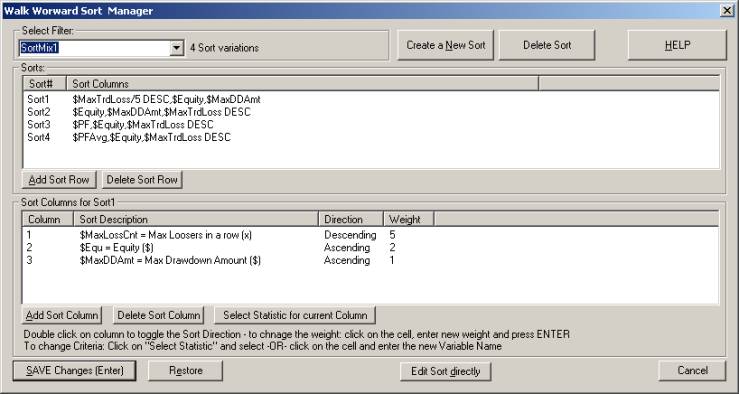

Each Sort Definition can contain one or several sort methods.

Below is an example of 4 different sorts:

Sort1=$MaxTrdLoss/5 DESC,$Equity,$MaxDDAmt

Sort2=$Equity,$MaxDDAmt,$MaxTrdLoss DESC

Sort3=$PF,$Equity,$MaxTrdLoss DESC

Sort4=$PFAvg,$Equity,$MaxTrdLoss DESC

Sort4=$PFAvg,$Equity,$MaxTrdLoss

DESC

Each WFA-Soft Definition is defined in a text file (Example

C:/BTWFMgr/SoftMix1.btwfs).

The “Walk Forward Sort Manager” is assisting you in managing and defining your

sort criterias:

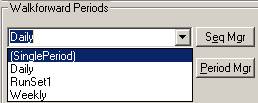

Walk Forward Analysis – Defining the Period Setup/Sequence

BTWFMgr

allows you several different ways to design the various in-sample(ISA) and

out-of sample(OSA) testing periods. BTWFMgr comes with many predefined period

setups,

but you can define and add any custom period setup!

To view the actual WFA period – click on ![]() (see examples below)

(see examples below)

You can even specify your own custom shift (in days) in the configuration:

Walk Forward Optimization/WFODayShift=0

a) Number of Walk Forward Runs and OSA Percent

You specify the number of Runs and the percent of out-of-sample days

Example: 10 Runs with 10% out-of-sample

b) Number of ISA/OSA Days

Example: 100 days ISA periods with 20 day out-of-sample periods

c)

Number of ISA/OSA Weeks

ISA periods always start on a Monday.

Example: 8 weeks ISA periods with 2 weeks out-of-sample periods

Defining a sequence of walk forward Period setups

BTWFMgr

allows you even to select a sequence of period setups,

so you can test which period setup performs the best for your strategies!

You can either select one of the predefined Period Sequences (Daily, Weekly

etc) –or-

design your own – press the “Seq Mgr” button – and the ”Walk Forward Period

Sequence Manager” will open!

The following functions are available:

a) Single Add: click one period on left – then click the Add button ![]()

b) Group Add: click

your selection on the left – then click the Add button ![]()

c)

All Add: click on the Add All button ![]()

d) Generate custom Sequence: enter the “Out-of-Sample(%)” and “Nbr of Runs”

list;

then click the “Generate a Walk Forward Sequence”

e)

Single Delete: click one period on right– then click the Delete button ![]()

f) All Delete: click

on the Delete All button ![]()

Remember to save any

newly created Period selection – press the Save putton:

![]() - then enter the new Period

Sequence Name.

- then enter the new Period

Sequence Name.

Walk Forward Analysis – Check your Save Result Options

Usually

all check boxes in the “Additional Diagnostic Options” section are left

unchecked

to achieved maximum speed for the Walk Forward Analysis:

In some cases you might want to review and track internal WFA calculations and

enable some diagnostic options, which are also saved to the new WFA sub folder.

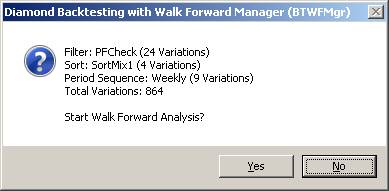

Walk Forward Analysis – Starting Walk Forward Analysis

To

finally start the Walk Forward Analysis (WFA) – simply press the green “Start

Run” button:

![]()

And

confirm the new Walk Forward Analysis Run:

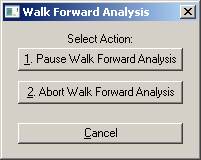

You can now abort or pause the WFA run by pressing the ![]() button.

button.

A

box appears were you can choose:

As

BTWFMgr calculates the many WFA permutations - the progress is shown to you in

the cyan bars

For

each level:

·

Filter

(current filter processed with in the current Date Range)

·

Range

(current Date Range within the current period)

Each period definition creates several date ranges for the

In-Sample/Out-of-Sample periods.

Click on “View Periods” to see the date ranges being created for the WFA

·

Period

(current Period as defined in the Period Sequence, unless a single period has

been selected)

·

Overall

progress at the button

Example

of running WFA:

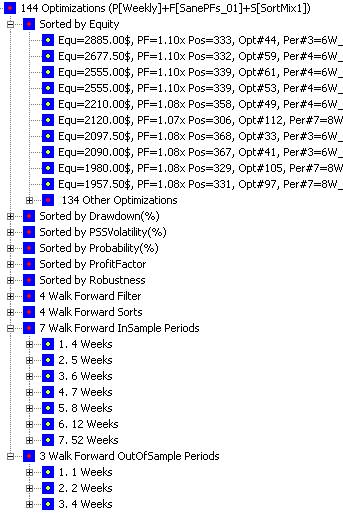

Walk Forward Analysis – Treeview Display

When

the WFA has completed, BTWFMgr automatically add a new tree branch, with blue

squares, at the top.

The

WFA results are shown first sorted by 6 different criteria (Equity, Drawdown,

Volatility, Probability, ProfitFactor and Robustness). Then follow the Filter

and Sort Variations used in this WFA and the In/OutSample periods calculated –

Below is an example:

Walk Forward Analysis – Result Viewing

BTWFMgr

offers many ways to view the WFA results and identify the best WFA logic:

View best WFA Equity

BTWFMgr

is showing by default the top 10 WFA results, just click on any of the results

to view the equity.

The remaining results are shown in the “XXX Other Optimizations” branch.

If you want to see more than 10 top results – changed the configuration

parameter “MaxWFOOpt”.

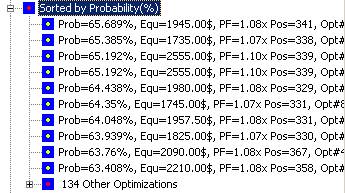

View best WFA Probability

Click

on the (+) in front of the “Sorted by Probability” branch and BTWFMgr will

expand the branch

and show the list of the top 10 results:

If

you want to see more than 10 top results – changed the configuration parameter

“MaxWFOOpt”

View best WFA Drawdown, Volatility, ProfitFactor and Robustness

Click

on the (+) in front of the “Sorted by XXX” branch and BTWFMgr will expand the

branch

and show the list of the top 10 results – similar to Equity and Probability.

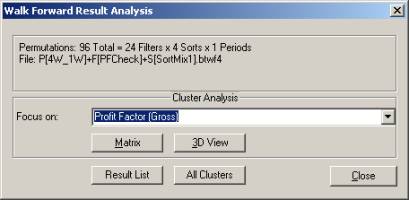

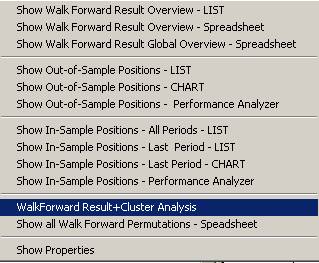

WFA 3D Cluster View

Right

click on any WFA results and you will see the WFA popup menu – then click on

”Walk Forward Result-Cluster Analysis” (or press Ctrl+A) or from the Menu

Function/Cluster Analysis:

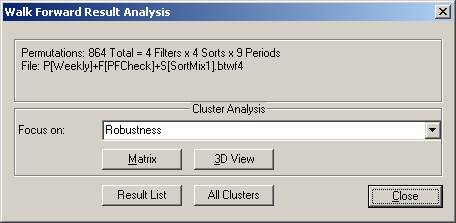

The Walk Forward Result+Cluster analysis box will appear:

Select

the criteria you would like to view (i.e. Net PL$) and click on “3D View”.

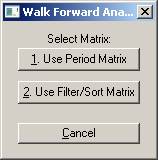

Now

you can choose if you want to plot the Filter and Sort variations –OR- In/OutSample

variations:

The

“Filter/Sort Matrix” will use the Filter and Sort variations for the X and Z axis.

The

“Period Matrix” will use the In/OutSample variations for the X and Z axis.

The

Y Axis is defined by your selected criteria abive.

Below

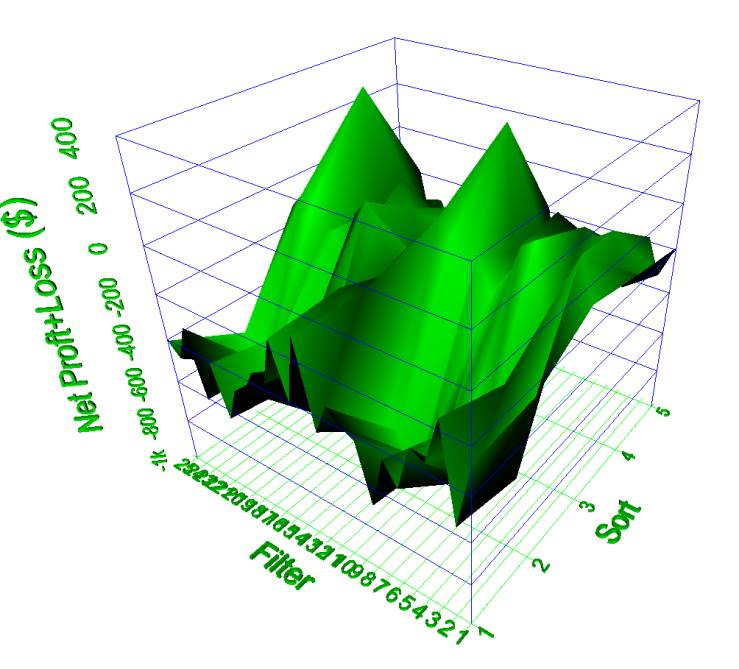

is an 3D WFA Result example, showing:

·

X

Axis: 4 sort variations plus the 5th Sort Average results

·

Z

Axis: 24 filter variations plus the 25th Sort Average results

·

Y

Axis: The Net Profit+Loss($) (or whichever criteria you selected)

Navigating the 3D View

·

To

Zoom in – rotate the mouse wheel away from you

·

To

Zoom out– rotate the mouse wheel towards you

·

To

Rotate to the left – click and hold left mouse button and move slowly to the

right

·

To

Rotate to the right– click and hold left mouse button and move slowly to the

left

·

To

Rotate to the top– click and hold left mouse button and move slowly down

·

To

Rotate to the bottom– click and hold left mouse button and move slowly up

·

To

move the center – click on hold the right mouse button and move in the desired

direction

·

To

capture/print the view – click on the print button in the toolbar

WFA Processing Details

Here

we give you a more detailed look at the actual steps the WalkForwardAnalysis

(WFA) process.

WFA will first create a new folder were all results are saved with the input

filename:

Example: Results for Input file:

“C:\BTWFMgr\PSS_RSISample\@ES\015Min_20080829_123503.btwf1”

are all saved to folder “C:\BTWFMgr\PSS_RSISample\@ES\015Min_20080829_123503”

The general WFAVerbose level determines the processing diagnostic details

level;

Which

all off for highest WFA Speed!

The

following abbreviations are used:

WFA=Walk Forward Analysis, ISA=In Sample Range, OSA=Out of Sample Range

The

following steps occur when for each WFA process:

·

Main1:

Load the period sequence definitions (from selected *.btwfl file, i.e.

Daily.btwfl)

·

Main2:

Check if for each period sequence definition enough data is present

·

Main3:

Create a matrix for each filter/sort and period variation

o Period1: Load next period

sequence definition (i.e. 10 Runs OSA 5%)

o Period2: Create the

In/OutSample date ranges – as shown in “View Periods” function

(i.e. create 10 date ranges for current data an OSA portion of 5%)

o Period3: Process the

first/next period definition

§ Range1: Process first/net

date range - create the subfolder for results:

Example: P001[30D_10D]+F[PFCheckTest]+S[SortMix1] = {PeriodFolder}

§ Calculate the statistics for

each Trade Permutation in the current ISA date range

§ Range2: Calculate the

relative ranking values

§ Range3: If requested

(SaveTrdPerm switch) export the statistics of each Trade Permutation to

the range result file in a sub folder for this period def, Example:

{PeriodFolder}/TradePermutations/ Rng0001_20080109_20080207.csv

§ Range4: Calculate the

specified filter condition to pass/fail each trade permutation

§ Range5: Sort the remaining

filtered candidates (unless ALL permutations filtered out)

§ Range6: If requested

(SaveOptPerm switch) exports the

{PeriodFolder}/Hits/OPT0000001_P001_F0001_S0001_20080109.csv

§ Range6: Establish the final

trade permutation ID

§ Range7: If requested

(SaveRunLog switch) exports the best result to:

{PeriodFolder}/Rng0001_20080109_20080207.csv

§ Repeat Range1-Range7 for all

remaining date ranges for this period

o Period4: Accumulate the OSA

Results and calculate the OSA statistics

o Period5: If requested

(SaveRunLog switch) exports the best result to:

{PeriodFolder}/ OPT0000008_P001_F0002_S0004.csv

o Repeat Period1- Period5 for

all remaining Period Definitions

·

Main4:

Save all WFA calculations to a binary file (*.btwf4)

·

Main5:

Post Process overall WFA Results

·

ll results are saved in a newly created folder – using the filename – Example:

WFA Results for: C:\BTWFMgr\PSS_RSISample\@ES\015Min_20080829_123503.btwf1

will be saved in new folder: “C:\BTWFMgr\PSS_RSISample\@ES\015Min_20080829_123503”

Within that folder the following sub folder are generated:

TradePermutations\P001_XXX – Results for Period Sequence #1

TradePermutations\P001_XXX\R0001_20080109_20080207_0000084Permutations.csv -

R0001=Range#1, 20080109=ISA Start Date, 20080207=ISA End Date

P[30D_10D]+F[PFCheckTest]+S[SortMix1] – WFA Results for:

Period “30D_10D” Filter “PFCheckTest” and Sort “SortMix1”

”SaveOptPerm” switch:

P[30D_10D]+F[PFCheckTest]+S[SortMix1]\Hits – WFA Filter Results

P[30D_10D]+F[PFCheckTest]+S[SortMix1]\Hits\SEQ0000001_P001_F0001_S0001_20080208.csv

SEQ0000001=Overall Sequence, P001=Period#1, F0001=Filter#1, S0001=Sort#1

20080208=ISA Start

”SaveRunLog” switch:

SaveRunLog

BTWFMgr Functions Reference

In

this section we illustrate in more detail how to use the various powerful

BTWFMgr functions.

Some functions might only apply only to Equity Mode (Equ) and/or Potential Mode

(Pot)

Long/Short Splitting (Equ)

After

you run an optimization, the results contains usually long and short trades in

the many permutations. BTWFMgr will detect the overall best Equity, Drawdown

etc using long and short

After

you run an optimization, the results contains usually long and short trades in

the many permutations. BTWFMgr will detect the overall best Equity, Drawdown

etc using long and short

and show them in the “Sort by XXX” green square branches:

In many cases you might need to split the long and short results into separate

files,

Thereby creating their own

Backtesting context with new “Sorted by XXX” lists!

Thereby creating their own

Backtesting context with new “Sorted by XXX” lists!

You

can do the L/S Split

by simply clicking on the LS

icon in the toolbar:

by simply clicking on the LS

icon in the toolbar:

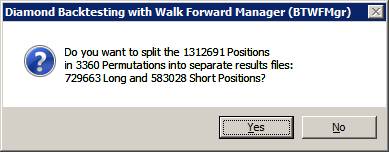

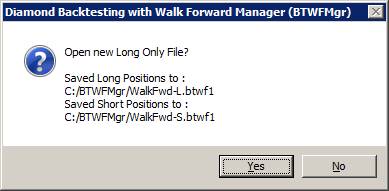

Next BTWFMgr will confirm

click

YES to continue:

Next BTWFMgr will proceed to generate

two new BTWFMgr result files,

And when finished, give you the option

to view the new “Long Only” (WalkFwd-L) result:

To view the “Short only” result – click on the new C:\BTWFMgr\WalkFwd-S.btwf1

file.

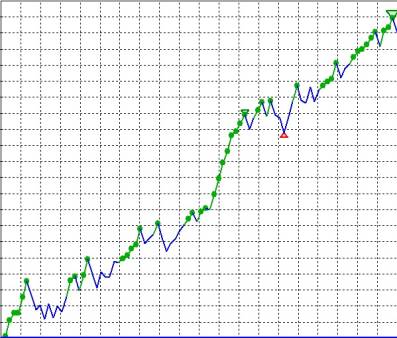

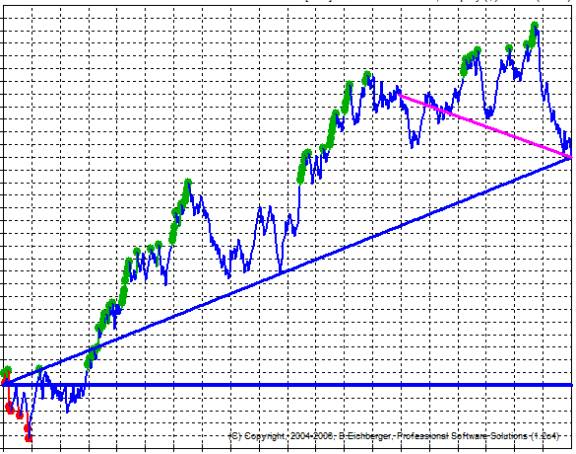

Equity Curve Cutoff (Equ)

BTWFMgr

(as most other software tools) sort all results by the ENDING Equity,

Which

is considered the best performance.

But

as you might have noticed, many times the best performance, is not always

continuing that previous performance – below is an example how a stellar

performance:

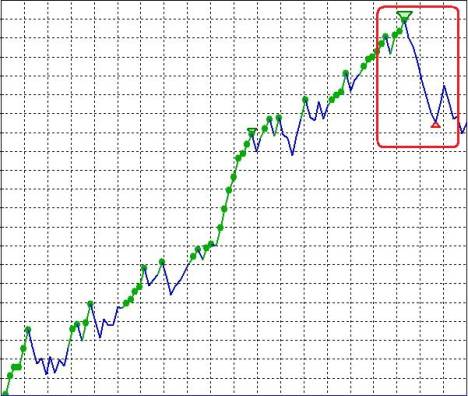

can

turn into a big drawdown

With

BTWFMgr you can now to double-check and research this phenomenon using your own

results.

Just define an earlier reference point within the equity curve – which is used

to sort the results,

instead of the usual 100% ENDING equity point.

In effect you virtually “cut off” a portion of last trades – just for the

sorting, the data Is not really lost.

(This

“cutoff” function only applies to the Equity Mode)

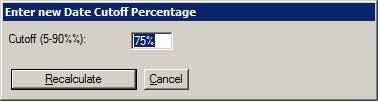

Simply click on the Recaclulate Icon:

![]()

Then

enter the new point of reference (instead of the usual 100% at the end):

To

start the conversion click “Recalculate”.

The new equity curves will show a new magenta line; connecting the cutoff point

with the ending result:

Click

on any performance result and you can easily check visually –

if

the previous performance actually continued.

This is similar to the the “In-Sample” and “OutSample” segments used in the Walk

Forward Analysis(WFA),

If the Equity results are using an early “cutoff” point

BTWFMgr will show the cutoff percentage in the header:

![]()

Export Statistics (Equ)

In

some cases you might want to use a custom spreadsheet, to identify and analyze

the backtesting trade permutations. BTWFmgr allows you to export all the

relevant statistical values for each permutation (or just the current one) to a

spreadsheet.

Simply right click on the permutation and select “Export Statistics”:

BTWFMgr

will generate

a new spreadsheet file for the current file – with StatsALL appended -

and ask you if you would like to view the new spreadsheet file (CSV format):

Click YES to see the

new spreadsheet, were you can now apply your custom analysis/sort etc:

This Statistic Export can also assist you in designing custom WFA filter

formulas!

Instead of all permutations you can also select the single export –for just the

current permutation.

Strategy Preparation

In order for BTWFMgr to analyze your strategy – BTWFMgr has to collect the

relevant data generated during your TradeStation®

Optimization runs.

To accomplish this BTWFMgr adds a small

section to the end of your EasyLanguage® strategy code.

Preparing TradeStation® - Opening your Strategy Code

Before BTWFMgr can automatically add the data collection section – open the strategy code:

·

Open TradeStation®:

Start/Programs/TradeStation 8.1 (Build XXX)

·

Close all workspaces

·

Open the strategy EasyLanguage Code

File/Open EasyLanguage Document (or Ctrl+E)

·

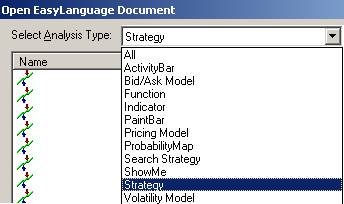

Select "Strategy" in the

Select Analysis type pull down list (at the top)

·

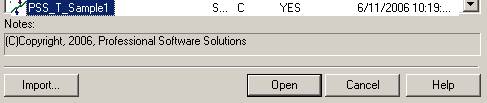

In the new list scroll down to your

Strategy and click the Strategy Name

then click on the Open button (as an example we use the PSS_T_Sample1 strategy

here …)

·

You might need to enter a protective

password to open the Strategy Code

·

A new Strategy EasyLanguage window has

opened:

![]()

Now we have

prepared TradeStation® for BTWFMgr to automatically modify your strategy.

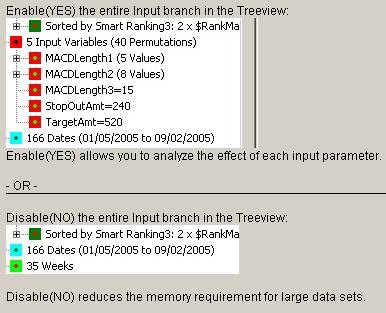

Adding the BTWFMgr Data Collection Section

·

Open BTWFMgr:

Start/Programs/Diamond Backtesting with Walk Forward Manager

(BTWFMgr)/Backtesting with Walk Forward Manager (BTWFMgr)

·

Once BTWFMgr has opened – click on the

cyan exclamation mark ![]() in

the tool bar:

in

the tool bar:

![]()

(or select File/Strategy Preparation from the Main Menu)

·

A new window will open – showing your

strategy name – click on Prepare:

·

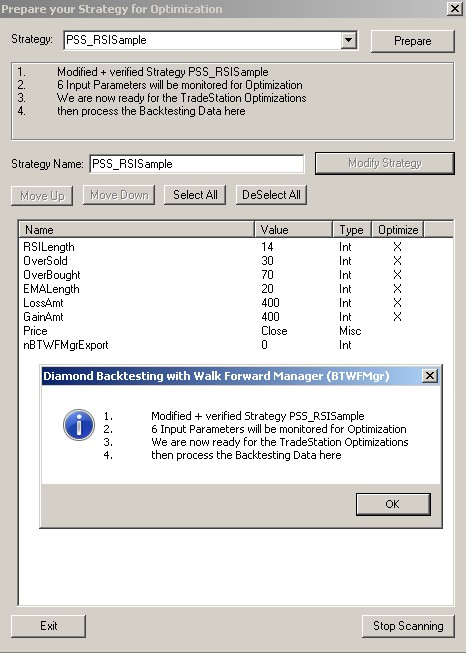

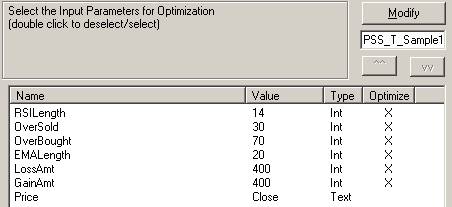

BTWFMgr is now presenting you with all

numeric strategy input parameter,

which can be included in the data collection during the TradeStation®

optimization:

(indicated by the X in the Optimization column)

Select ALL inputs you might use in any TradeStation® optimization (usually

all).

Just double click on the input row and BTWFMgr will select/deselect it.

·

You can change the sequence of an input

with the up ![]() and down

and down ![]() button

button

·

Now click on the modify button to let

BTWFMgr add the new data collection section

![]()

·

Now BTWFMgr will automatically modify

the strategy code for you and

after a few seconds show the confirmation box – click on OK:

·

Now you are ready to run the regular

TradeStation® Optimization on your strategy,

which will now collect the relevant data for you, so you can then analyze it in

BTWFMgr.

The initial Strategy Potential mode (nBTWFMgrExport=1) is automatically

pre-selected for you.

Below is a sample of the BTWFMgr data collection section.

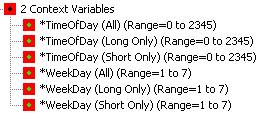

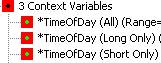

Adding Context Variables

When you develop your strategy, you

usually want to research also the effect of additional context input values on

the overall results. With BTWFMgr you can now check if certain ranges or values

will improve the overall strategy results and by filtering out bad entries.

BTWFMgr adds for you automatically already the TimeOfDay context value.

Example:

Research of a certain range of the moving average angles might be connected to

better results.

Below are the steps to add an additional context variable:

·

Add Context Variable Name

Add one line for each new context variable after the line

WalkForwardVar = WalkForwardVar + "/*TimeOfDay";

Here is one example - adding an angle:

WalkForwardVar = WalkForwardVar + "/ExpAngle";

(the * indicates the first context variable name):

·

Increase Argument Counter

Increase the input counter by the number of newly added context values,

below the line:

arrPSSBTVal[0] = 6; // Number of tracked Strategy Inputs

if nBTWFMgrExport = 1 OR (nBTWFMgrExport = 3 AND CurrentShares = 1818) then

arrPSSBTVal[0] = 7; // add Number of

Context Variables

In our example: we increase by one - from 7 to 8

·

Add Context Variables to

Function Call

Add the actual context values to the BTWFMgr data capture function argument

list, after the line:

arrPSSBTInp[6] = Time; // Context Input#01

Here is one example - adding an angle:

arrPSSBTInp[7] = AnglePercent; // Context Input#02

·

Verify the EasyLanguage

After modifying he strategy code verify the EasyLanguage code (Tools/Verify)

·

Re-Run TradeStation®

optimization

Now you can re-run the TradeStation® Optimization,

which will now collect also the data at each entry also the added context

variable values.

More information at: http://www.profsoftware.com/bt/eldmode.htm

BTWFMgr will show the result for each context variable in the "Context

Variables" section.

Sample of Data Collection Section

Below is a sample of the BTWFMgr data

collection section – with the two added context variables:

Time, // Context Input#01

AnglePercent, // Context Input#02

//====== BTWFMGR_F2D83D3A_BBDB_447E_B0FE_209ED95E4E3F

=============

//====== WALK-FORMWARD-OPTIMIZATION DATA COLLECTION

SECTION ======

Vars: nRetWFO(0),WalkForwardVar("");

if nBTWFMgrExport > 0 then begin

if GetAppInfo(aiOptimizing) = 1 then begin

if

WalkForwardVar = "" then begin

WalkForwardVar

= "RSILength";

WalkForwardVar = WalkForwardVar + "/OverSold";

WalkForwardVar = WalkForwardVar + "/OverBought";

WalkForwardVar = WalkForwardVar + "/EMALength";

WalkForwardVar = WalkForwardVar + "/LossAmt";

WalkForwardVar = WalkForwardVar +

"/GainAmt";

if

nBTWFMgrExport = 1 then begin

WalkForwardVar = WalkForwardVar + "/*TimeOfDay";

WalkForwardVar = WalkForwardVar + "/ExpAngle";

end;

end;

if

nBTWFMgrExport = 2 then begin

nRetWFO = PSS_F_WFO10("PSS_T_Sample1", //Strategy

WalkForwardVar,

// Names of Inputs

6,

// each selected Input Variable below

RSILength, // Strategy Input#01

OverSold,

// Strategy Input#02

OverBought,

// Strategy Input#03

EMALength,

// Strategy Input#04

LossAmt, // Strategy

Input#05

GainAmt

// Strategy Input#06

,0,0,0,0);

end;

if

nBTWFMgrExport = 1 then begin

nRetWFO = PSS_F_WFO10("PSS_T_Sample1", //Strategy

WalkForwardVar, // Names of Inputs

-8,

// each selected Input Variable below

RSILength,

// Strategy Input#01

OverSold, // Strategy Input#02

OverBought,

// Strategy Input#03

EMALength,

// Strategy Input#04

LossAmt,

// Strategy Input#05

GainAmt, // Strategy

Input#06

Time,

// Context Input#01

AnglePercent, // Context Input#02

0,0);

end;

end;

If

nBTWFMgrExport = 1 then begin

If

marketposition = 1 then

Sell ("Lbt") next bar Market;

If

marketposition = -1 then

Buy to Cover ("Sbt") next bar Market;

end;

end;

//======

BTWFMGR_F2D83D3A_BBDB_447E_B0FE_209ED95E4E3F =============

Detecting the optimal Strategy Potential/Parameters

After

you have prepared your strategy and the TradeStation Optimization has

completed,

BTWFMgr will automatically starts and perform automatically the initial data

conversion and then

present to you the Strategy Potential Analysis. (make sure you have

nBTWFMGrExport set to 1).

Analyzing the Strategy Per Trade Potential

Analyzing

the Strategy Per Trade Potential

Analyzing the Strategy Yearly Potential

Analyzing

the Strategy Yearly Potential

Analyzing the Strategy Parameter Potentials

Analyzing

the Strategy Parameter Potentials

Analyzing the Strategy Context Variables

Analyzing

the Strategy Context Variables

(under

construction …)

·

Exit Optimization Results

Showing the top 10 results - sorted by the best average return per trade:

![]()

·

The remaining results are collected behind the “Other Exit

Optimizations” item:

![]()

How many exit optimizations are shown is defined in

the “MaxExitResults” configuration parameter (2000) in the TreeView section.

·

Exit Parameter Analysis

Showing for each exit parameter the individual results

Detecting the optimal Strategy Exit Method

After

you have identified the best Strategy Potential for Long and Short trades,

you can now let the “Position Exit Manager (PEM)” calculate many

different exit scenarios,

so you can identify the best

“Strategy Exit Logic”.

so you can identify the best

“Strategy Exit Logic”.

Usually Longs and Shorts have different optimal exit parameters.

Since the integrated “Position Exit Manager (PEM)” is using fast object

oriented C++ code,

it can process 100,000 exit variations per second (~1000 time faster than the

regular backtesting)!

First click on the result with the best potential, which actualizes the

permutation ID.

Then Click on the ![]() button in the

toolbar, which brings up the Optimization box:

button in the

toolbar, which brings up the Optimization box:

The current permutation ID (1018) is shown in:

![]()

which

determines all the positions to be tested.

Then

click on ![]() to create a new

default template tailored to the current potential.

to create a new

default template tailored to the current potential.

This will create a new exit definition:

![]()

Each line defines a type of exit with a testing range

(see details about exit types below).

You can select various processing parameters:

Finally you start the processing – click on:

![]()

Which

will process the 180,224 exit permutations

for each of the 579 positions in Trade Perm ID 1018

![]()

In

only a few minutes all 88.4 million scenarios are completed:

![]()

![]()

Analyzing the Strategy Exit Results

After

the optimization is complete a new exit result branch will appear in the

treeview:

Analyzing the Strategy Exit Parameters

Analyzing

the Strategy Per Trade Potential

BTWFMgr Configuration and Preferences

BTWFMgr

allows you to easily change and almost all of its internal parameters,

so you can tailor the behavior to your needs.

To start the configuration, simply click on the ![]() icon in the toolbar –or- Ctrl+C

–or-

icon in the toolbar –or- Ctrl+C

–or-

select or from the in the Menu: File/Backtesting Configuration and Preferences

(Ctrl+C)

All parameters are organized by topics:

·

TreeView

·

Smart Ranking Analysis

·

Best Trade Permutation Analysis

·

Walk Forward Optimization

·

Strategy Potential & Probability

Analysis

·

Initial Data Conversion

·

Position Exit Manager (PEM)

·

General

·

Chart

Below

each topic the associated parameters are attached. You can expand and collapse

each topic,

by clicking on the plus or minus mark (![]() and

and ![]() )

in front of the topic.

)

in front of the topic.

To

see a more detailed description - click on the parameter,

and the right window section will show the description and current setting -

You can now:

·

Change the parameter value (simply

enter/select the new value and click on “Apply”)

·

Restore to the previous setting – after

an erroneous change for example – click on “Restore”

·

Switch to the parameter default value –

click on “Default”

Close

the Configuration Window via the “Close” button, the ESC key or the ![]() window button.

window button.

The

new parameter settings is shown with a star and activated next time you open

BTWFMgr again.

A detailed description of each parameter section is presented below.

Below is a sample screen of the BTWFMgr Configuration and Preference WindowBelow is a list of all the available BTWFMgr Configuration settings you

can adjust to your needs.

(You can also edit the configuration parameters directly in the C:/BTWFMgr/BTWFMgr.ini

file)

TreeView Settings