Now BTWFMgr is also available for the AmiBroker

platform!

The following topics are available for BTWFMgr and AmiBroker:

The location were the "Diamond Backtesting with Walk Forward Manager"

will be installed is:

"C:\BTWFMgr"

Compare AmiBroker and BTWFMgr

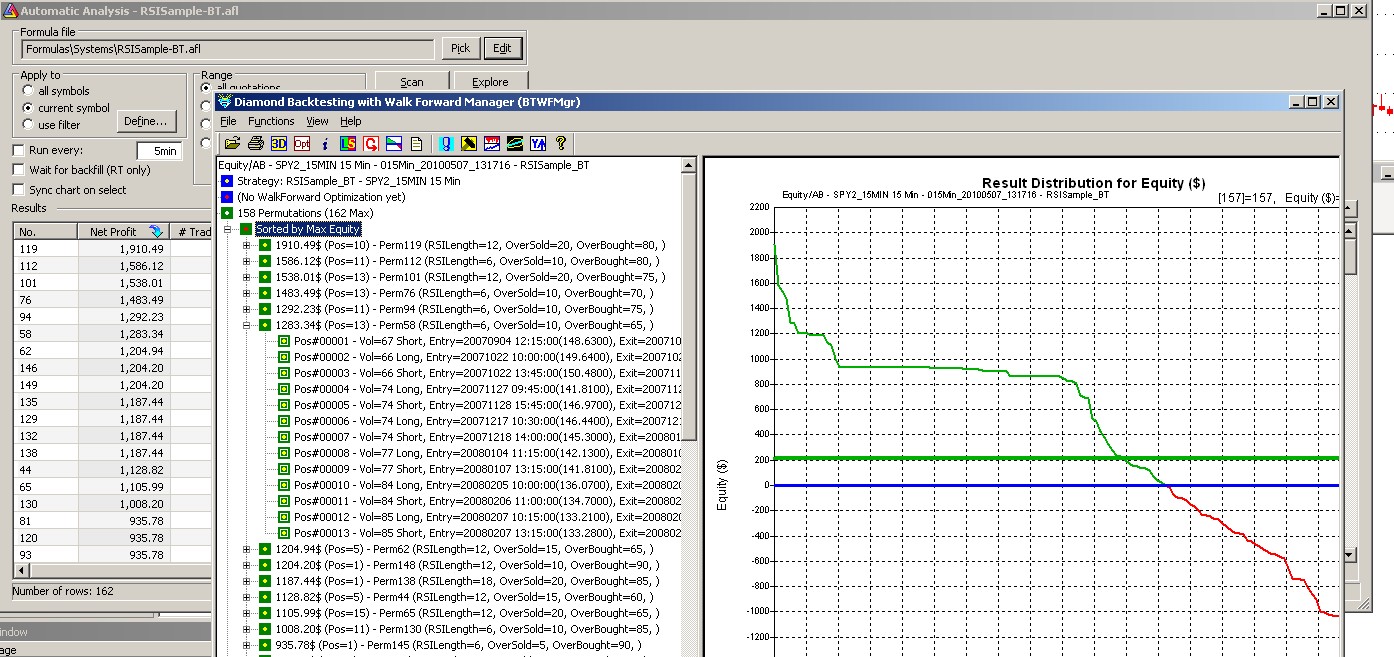

BTWFMgr replicates the exact equity and performance as shown in AmiBroker when

you run an optimization or backtest!

In this example the top equity results (1910.40, 1586.12, 1538.01 etc) match the

"Diamond Backtesting" window,

which shows also a distribution of all the equity results and the average equity

(around $200):

(Internally BTWFMgr is setting the CalcPL switch in the

"Initial conversation" config section to YES)

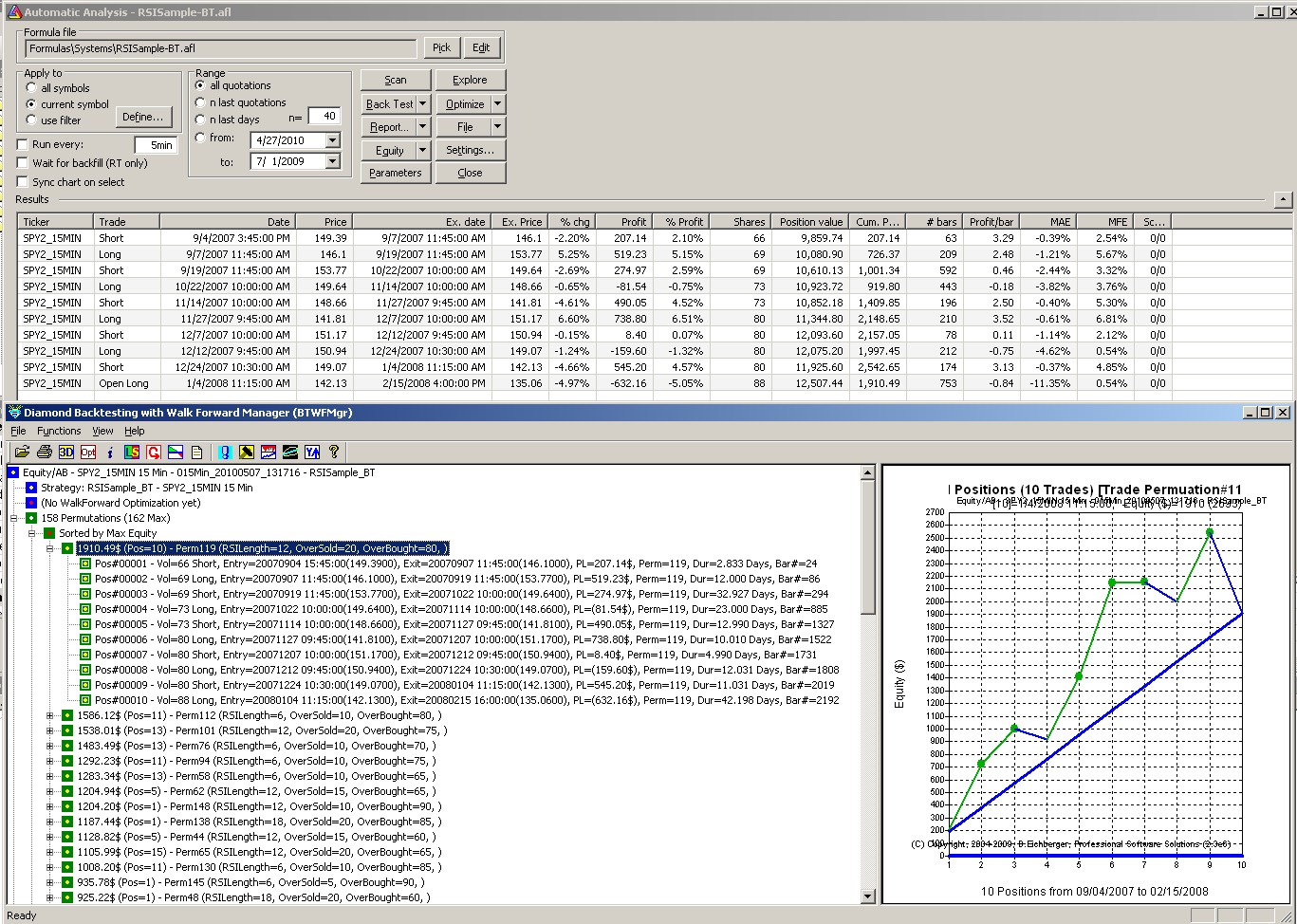

Equity Graph

You can also instantly view and analyze EACH backtesting equity graph/result

instantly

by clicking in

the green permutation icon ($1910.49) and even see each position as shown below:

Ho to prepare your System/Strategy in

AmiBroker (AB)_Prep)

In order to use the powerful BTWFMgr functions - you have to convert your AmiBroker System/Strategy

in this simple step.

a) Start the "AmiBroker BTWF Code Preparation" utility

Start/Programs/Amibroker Backtesting with Walk Forward Manager (BTWFMgr)/Amibroker_BTWF_Code_Prepapartion

-OR-

click in BTWFMgr on Functions/Prepare your Strategy for BTWFMgr -OR-

click on the blue exclamation mark icon the BTWFMgr icon

b) When the "AmiBroker BTWF Code Preparation" opened - select the system

you want to prepare for optimizations:

Automatically the different Input names are shown the system is using.

c) Click on the "Prepare" button

d) Choose from:

YES=Replace the converted/prepared system AFL file

NO=Create a new converted/prepared system AFL file with "-BT" added to

the filename

Cancel=stop the preparation process

e) View converted File

If the "Show File" box is enabled the program

will automatically display the

converted AFL file (RSICross.afl)

AFL "Optimize" code lines

The prepapartion program (AB_Prep) will automatically scan all the AFL files in

the Formula folders

and select all the systems which contain lines like:

Variable = Optimize ( "Name",

Default,...);

Example:

RSILength = Optimize("RSILength", 11, 6, 20, 1 );

RSIValue = RSI(RSILength);

Note that you should always use variables before using the optimize parameter in

the code as shown above,

so that the program can pass on the value of the variable to the data collection

module!

NOT LIKE THIS:

RSIValue = RSI(Optimize("RSILength", 11, 6, 20, 1 ));

AFL "Optimize" section begin/end declaration

You can instruct AB_Prep to only seach for Input variables in a specific section

by

surrounding your section with all the Optimize functions with the "//BTWF_START"

and "//BTWF_END" comments:

Example:

//BTWF_START

RSILength = Optimize("RSILength", 11, 6, 20, 1 );

OverSold = Optimize( "OverSold", 20, 5, 40, 5);

OverBought = Optimize( "OverBought", 70, 60, 90, 5 );

//BTWF_END

AFL single bo.Backtest(True) declaration

Note that AmiBroker permits only ONE instance of

the "bo.Backtest(True)" function,

so when the scanner already detects this instructions

above the data collection section,

it will automatically turn the default instruction in the data collection

section into a comment with the line reference:

Example:

if (Status("action") == actionPortfolio )

{

bo = GetBacktesterObject();

// bo.Backtest(1); // already called at Line#783

Stratregy Input Parameter Synchronization from

BTWFMgr to AFL file

Added AmiBroker AFL synchronization - using the #include_once function:

a) Right-click on the permutation and select "Synchronize Strategy

Parameter"

![]()

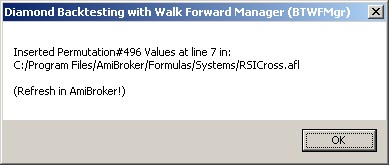

b) BTWFMgr will export all parameter for this permutation to a new AFL file,

which is included after the last "Optimize()" statement or //BTWF_END

command:

//BTWF_END

#INCLUDE_ONCE "C:/Program Files/AmiBroker/Formulas/Systems/RSICross-Perm.afl"

//Inserting Parameter Values for Perm#747

c) A new AFL file is created with the exported values for the

selected permutation (RSICross-Perm.afl):

//BTWFMgr strategy permutation parameter section for Permutation#747

EnableTextOutput(False);

RSILength = 14; //Input#001

OverSold = 15; //Input#002

OverBought = 90; //Input#003

EnableTextOutput(True);

d) A confirmation box appears:

Import SPY 15Min test Data

We have also supplied a sample SPY 15Min intraday data series (SPY15MIN.TXT)

Copy the sample SPY 15Min intra-day data series (SPY15MIN.TXT)

to the main AmiBroker folder:

C:\Program Files\AmiBroker\SPY15MIN.TXT

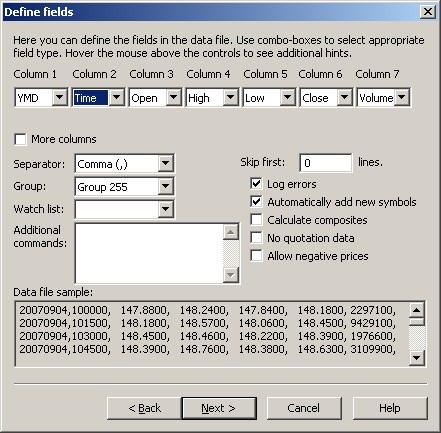

To Import this file into AmiBroker:

a) Click on File/Import Wizard

b) Click on PICK FILES and select "C:\Program

Files\AmiBroker\SPY15MIN.TXT".

c) Click NEXT

d) Adjust the settings as shown below:

e) Click on NEXT

f) If you would like you can save these import settings

g) Click on FINISH

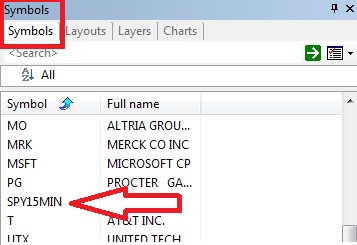

h) You should see a new Symbol in the "Symbol" Tab: SPY15MIN

i) To see the intraday data use: View/Intraday/15 Min

Diagnostics/DateConversions in Data Collection Module

The new 1.4 version will show you the current date format used by AmiBroker (and

the computer in general) in the log file - Example:

BT-AB |18:51:42.411b|Detecetd DateFormat: M/D/YYYY (Day=2, Month=1, Year=3)

The module will show you the fields were it detected

the Day, Month and Year:

(Day=2, Month=1, Year=3)

in the UK for example you would see:

BT-AB |18:54:39.886b|Detecetd DateFormat: DD/MM/YYYY (Day=1, Month=2, Year=3)

The module will show you the fields were it detected

the Day, Month and Year:

(Day=1, Month=2, Year=3)

This diagnostic logfile is at:

C:\BTWFMgr\logs\YYYYMMDD\PSS_AB.log

(YYYYMMDD = current date - 20110514 = May 14th, 2011)

Each new data collection sequence starts with:

INIT |11:44:14.968 |====== Opening C:/BTWFMgr/logs/20110514/PSS_AB.log ======

Each 100th trade/position AmiBroker sends to BTWFMgr is

shown with the Pos: Marker:

BT-AB |18:51:42.412b|Pos#000001: Entry: $ 148.72 9/4/2007 1:00:00 PM (20070904130000) Exit: $ 135.06 2/15/2008 4:00:00 PM (0) Size= 67 Par= 6, 5, 60

BT-AB |18:51:43.387b|Pos#000101: Entry: $ 154.90 10/15/2007 11:45:00 AM (20071015114500) Exit: $ 154.37 10/17/2007 10:45:00 AM (0) Size= 60 Par= 7, 15, 60

BT-AB |18:51:43.670b|Pos#000201: Entry: $ 152.55 10/19/2007 10:30:00 AM (20071019103000) Exit: $ 150.15 10/22/2007 2:00:00 PM (0) Size= 62 Par= 6, 20, 60

...

The "Entry:" Shows the entry price "$ 148.72" and entry date

and time as text received from AmiBroker "9/4/2007 1:00:00 PM"

and the converted numeric entry (20070904130000)

The "Exit:" Shows the entry price "$ 135.06"

and entry date and time as text received from AmiBroker "2/15/2008 4PM"

and the converted numeric entry (20080215160000

The "Par=" entry shows the respective first 3 strategy input parameters (RSILength,

OverSold/Bought)

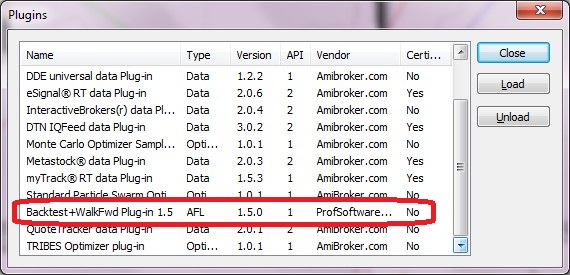

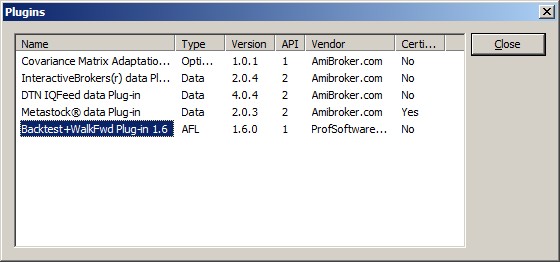

When you pull up the plug in list (Tools/Plugins) you should see the 1.4 version:

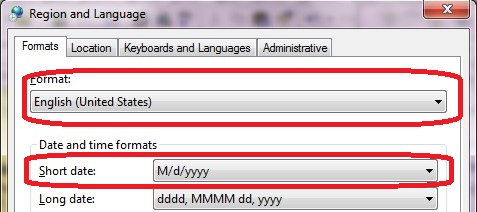

Set the date format in Start/Control Panel/Clock, Language, and Region/Change

the date, time or number format:

(Always select formats with slashes as delimiter! - never a minus)

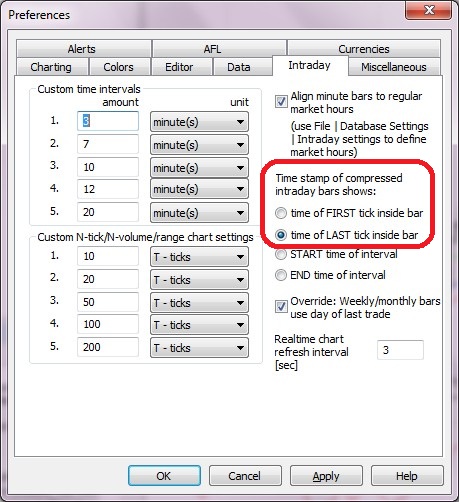

Expected AmiBroker Settings

Make sure you have the "Time Stamp" set to "time of LAST tick

inside bar":

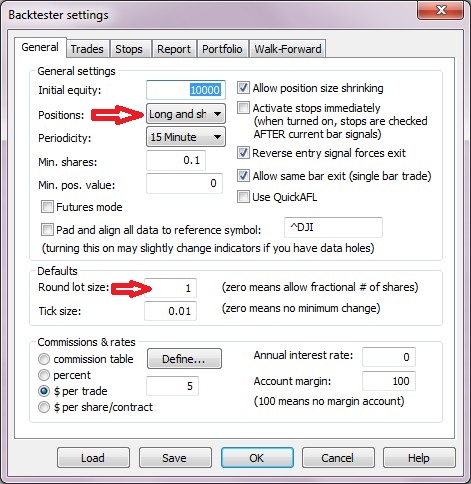

And "Backtester Settings" as shown below (set Commission as you see

fit):

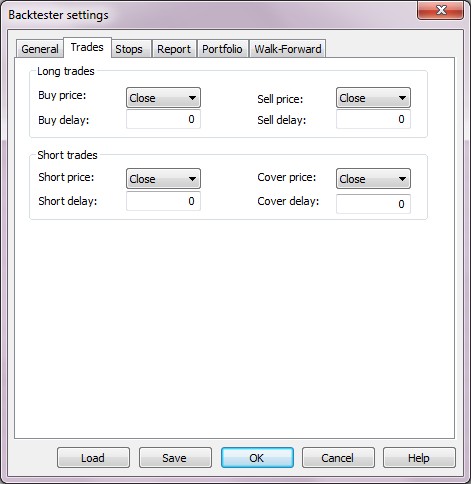

Suggested Trade Settings:

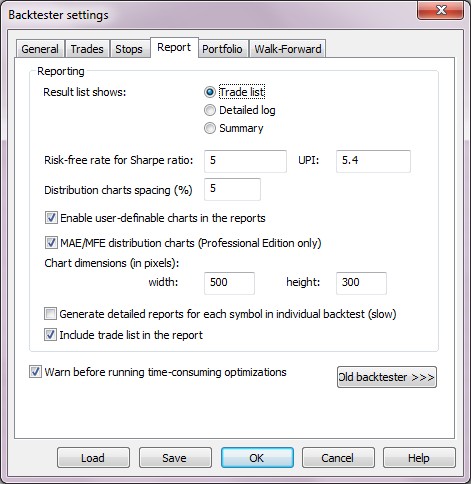

Suggested Report Settings:

"Diamond Backtesting with Walk Forward Manager (BTWFMgr)" Main Page

© Copyright 2004-2011, Burkhard Eichberger, Professional Software Solutions

All Rights Reserved Worldwide.

xx

xx